Fill Out a Valid Vermont S 3 Form

Fill Out a Valid Vermont S 3 Form

In the picturesque state of Vermont, nestled among the Green Mountains, there lies a critical piece of documentation for buyers and sellers alike: the Vermont S 3 form, otherwise known as the Sales Tax Exemption Certificate for purchases for resale and by exempt organizations. This form, far from being just another piece of bureaucracy, serves as a lifeline for various entities, enabling transactions free from sales tax under certain conditions. Whether it’s a single purchase with a clear-cut purchase price or multiple purchases where the exemption is intended to apply over time, this document details meticulously the nature of the transaction. Businesses, along with specific nonprofit organizations recognized under IRS code 501(c)(3) for their religious, educational, or scientific purposes, find themselves navigating this form to assert their exemption. Government units, both federal and Vermont-based, along with volunteer fire departments, ambulance companies, and rescue squads, are also among those who benefit. Significantly, the document emphasizes the importance of "good faith" acceptance by sellers, a concept rooted in an understanding of and compliance with the law, to facilitate these exempt transactions. Moreover, the form encapsulates instructions for its use, emphasizing its inapplicability to contractors and the necessity of retaining it for records. The paths for exemption claims are clearly delineated, offering a beacon of guidance through the often complex landscape of tax exemptions. As such, the Vermont S 3 form stands not just as a procedural necessity, but as a testament to the intricate dance between taxation laws and the entities seeking solace under its exemptions.

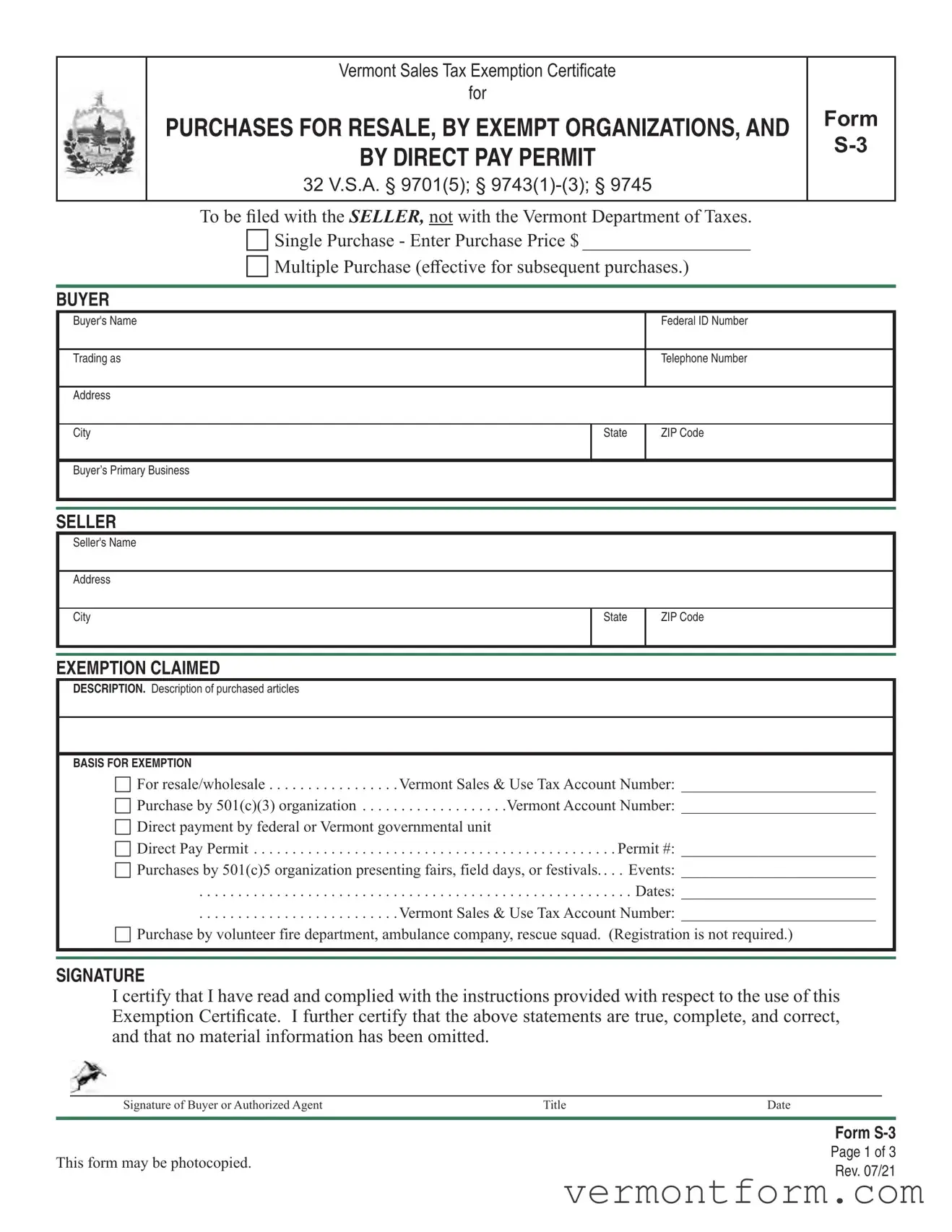

Vermont Sales Tax Exemption Certificate

for

PURCHASES FOR RESALE, BY EXEMPT ORGANIZATIONS, AND

BY DIRECT PAY PERMIT

32 V.S.A. § 9701(5); §

FORM

To be filed with the SELLER, not with the Vermont Department of Taxes.

Single Purchase - Enter Purchase Price $ __________________

Multiple Purchase (effective for subsequent purchases.)

BUYER

Buyer's Name |

|

Federal ID Number |

|

|

|

Trading as |

|

Telephone Number |

|

|

|

Address |

|

|

|

|

|

City |

State |

ZIP Code |

|

|

|

Buyer’s Primary Business |

|

|

|

|

|

|

|

|

SELLER

Seller's Name

Address

City |

State |

ZIP Code |

|

|

|

|

|

|

EXEMPTION CLAIMED

DESCRIPTION. Description of purchased articles

BASIS FOR EXEMPTION |

|

|

For resale/wholesale |

Vermont Sales & Use Tax Account Number: _________________________ |

|

Purchase by 501(c)(3) organization |

. . . . . . . . . . . . . .Vermont Account Number: _________________________ |

|

Direct payment by federal or Vermont governmental unit |

|

|

Direct Pay Permit |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

Permit #: _________________________ |

Purchases by 501(c)5 organization presenting fairs, field days, or festivals. . . |

. Events: _________________________ |

|

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . Dates: _________________________ |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

Vermont Sales & Use Tax Account Number: _________________________ |

|

Purchase by volunteer fire department, ambulance company, rescue squad. (Registration is not required.)

SIGNATURE

I certify that I have read and complied with the instructions provided with respect to the use of this Exemption Certificate. I further certify that the above statements are true, complete, and correct, and that no material information has been omitted.

Signature of Buyer or Authorized Agent |

Title |

Date |

Form

This form may be photocopied. |

Page 1 of 3 |

|

Rev. 07/21 |

||

|

FORM

Vermont Sales Tax Exemption Certificate for

Purchases for Resale, by Exempt Organizations, and by Direct Pay Permit

This exemption certificate does not apply to contractors.

General Information

Please print in BLUE or BLACK ink only.

This exemption certificate applies to the following:

•Purchase(s) of tangible personal property for the purpose of resale

•Purchase(s) by an organization which is designated as a 501(c)(3) by the Internal Revenue Service, or agricultural organizations qualified for exempt status under § 501(c)(5) when presenting agricultural fairs, field days, or festivals

•Purchase(s) by a Federal or Vermont governmental unit (direct payment)

•Purchase(s) using a Direct Pay Permit

•Purchase(s) by a volunteer fire department, ambulance company, or rescue squad

Please note: Civic, social, recreational, and business league organizations are not 501(c)(3) organizations, and therefore cannot make exempt purchases.

Accepting an Exemption Certificate in “Good Faith”

The buyer must present to the seller an accurate and properly executed exemption certificate for the exempted sale. The responsibility is on the seller to determine if the buyer is submitting the exemption certificate in “good faith.” This requires the seller to be familiar with Vermont Sales and Use Tax law and regulations, including exemptions, that apply to the seller’s business. If the buyer provides a certificate that is not valid, i.e., the item purchased does not qualify for the exemption, this is not in good faith and the seller should not accept the certificate. When the seller accepts the certificate in good faith, the seller is not liable for collecting and remitting Vermont Sales Tax.

An exemption certificate is received at the time of sale in good faith when all of the following conditions are met:

•The certificate contains no statement or entry which the seller knows, or has reason to know, is false or misleading.

•The certification is on an exemption form issued by the Vermont Department of Taxes or a form with substantially identical language.

•The certificate is signed, dated and complete (all applicable sections and fields completed).

•The property purchased is of a type ordinarily used for the stated purpose, or the exempt use is explained.

Form

Page 2 of 3 Rev. 07/21

Burden of Proof

The burden of proof is on the seller to demonstrate the certificate was taken in good faith. If the seller cannot provide an exemption certificate showing that the sale was exempt, the Department will seek to collect tax from the seller. If, however, the seller can prove the buyer’s claim for the exemption was false, the Department will seek to collect the tax from the buyer.

Obtaining the Exemption Certificate

The seller must obtain an exemption certificate from the buyer either prior to or at the time of the sale. If the certificate is not available at the time of sale, the seller has 90 days after the sale to obtain a fully executed certificate, accepted in good faith.

Retaining the Exemption Certificate

Sellers must retain exemption certificates for at least three years from the date of the last sale covered by the certificate to document why the tax was not collected from the buyer.

Multiple Purchase Exemption Certificates

If the buyer presents a “Multiple Purchase” exemption certificate to the seller, it may be used only when purchasing tangible personal property for use as indicated on this exemption certificate. For each purchase covered by the exemption certificate, the sales slip or invoice must show the buyer’s name and address sufficient to link the purchase to the exemption certificate on file.

Other types of exemption certificates that may be applicable are available on our website at

For questions regarding how these exemption certificates may be properly applied, please contact the Vermont Department of Taxes at (802)

Form

Page 3 of 3 Rev. 07/21

| Fact | Detail |

|---|---|

| Form Purpose | Used for Vermont Sales Tax Exemption Certificates for purchases for resale and by exempt organizations. |

| Governing Laws | 32 V.S.A. § 9701(5); § 9743(1)-(3) |

| Submission Requirement | Must be filed with the seller, not with the VT Department of Taxes. |

| Types of Exemptions | Includes exemptions for resale/wholesale, purchases by 501(c)(3) organizations, direct payments by Federal or Vermont governmental units, and purchases by volunteer fire departments, ambulance companies, or rescue squads. |

| Proper Use Conditions | Exemption certificates must be presented prior to or at the time of purchase, must be complete and accurate, and must meet all conditions outlined in published instructions for acceptance in good faith. |

Filling out the Vermont Form S-3 is a simple yet critical task for buyers looking to claim exemption from sales tax on purchases for resale or for eligible organizations. Proper completion ensures compliance with tax regulations and enables a seamless transaction free from unnecessary tax costs. Here's a step-by-step guide to fill out the form correctly:

Once the Form S-3 is properly filled, it should be provided to the seller and not sent to the Vermont Department of Taxes. It's important to keep in mind that retaining copies of completed exemption certificates and ensuring their accuracy is crucial for both buyer and seller to meet tax regulations and to defend the exemption in case of audits. Remember, this form is pivotal for documenting the tax-exempt status of qualifying purchases, thereby facilitating a smoother operation for eligible buyers and sellers in adherence to Vermont tax laws.

What is the Vermont S-3 Sales Tax Exemption Certificate, and who should use it?

The Vermont S-3 Sales Tax Exemption Certificate is a document that qualifies certain purchases for exemption from Vermont sales tax. This exemption applies specifically to purchases of tangible personal property intended for resale, purchases made by certain 501(c)(3) organizations (religious, educational, or scientific), direct payments by Federal or Vermont governmental units, and purchases made by volunteer fire departments, ambulance companies, or rescue squads. This certificate is crucial for retailers or organizations that meet these criteria and wish to make tax-exempt purchases in compliance with Vermont law.

How do buyers properly apply for a tax exemption using the Vermont S-3 form?

To appropriately apply for a tax exemption with the Vermont S-3 form, the buyer should first ensure that their purchase qualifies under one of the exempt categories mentioned. Upon confirming this, the buyer must accurately complete the form with all required information, including their Federal ID Number, business name, address, the specific basis for exemption claimed, and a detailed description of the purchased articles. It's imperative that the form is filled accurately and completely to avoid any discrepancies and to ensure the exemption is granted. The buyer must then provide this form to the seller prior to or at the time of purchase. It's worth noting that sellers are required to accept these certificates in "good faith," based on the belief that the information provided on the certificate is accurate and applicable to the law.

What are the responsibilities of sellers who accept the Vermont S-3 Exemption Certificate?

Sellers who accept the Vermont S-3 Exemption Certificate have several responsibilities to ensure compliance with Vermont tax laws. Firstly, sellers must verify that the certificate is fully and accurately completed and presented before the time of sale. They should also assess the certificate's information in "good faith," which involves an educated assumption that all details are accurate and comply with current laws and regulations. Sellers are obligated to retain a copy of the exemption certificate for at least three years from the date of the last sale covered by the certificate. This retention is necessary for documentation purposes, should any tax-related inquiries arise. Moreover, sellers must ensure that the specific purchases linked to the exemption certificate strictly adhere to the criteria outlined for tax-exempt purchases.

What happens if a Vermont S-3 Exemption Certificate is used incorrectly?

Incorrect use of the Vermont S-3 Exemption Certificate can have serious consequences for both buyers and sellers. If it's determined that a certificate was used for purchases that do not qualify for tax exemption, the buyer could be held liable for the unpaid taxes, in addition to penalties and interest. For sellers, accepting a certificate known to be used improperly can result in the obligation to pay the applicable sales tax, plus potential penalties and interest. Sellers must exercise due diligence in accepting exemption certificates by ensuring they are completely and accurately filled out and that the items purchased align with the exempt purposes stated on the certificate. It is crucial for both parties to understand the rules and regulations governing tax-exempt purchases to avoid any misuse of the exemption certificate.

When filling out the Vermont S-3 form, commonly encountered mistakes can lead to unnecessary delays or even rejection of the exemption claim. Paying close attention to detail and ensuring accuracy is paramount. Here are five errors frequently made:

For the form to serve its purpose effectively, all the above elements must be meticulously filled out. It's also essential to keep a copy of the completed form for record-keeping and to give the original to the seller for their records. This not only ensures compliance but also facilitates a smoother transaction process, free from potential tax liabilities.

When dealing with the Vermont S-3 form, various other documents and forms often come into play, especially for organizations and businesses seeking tax exemptions or conducting tax-exempt purchases. Understanding these documents can be helpful for a smooth and compliant transaction process.

Each of these documents plays a critical role in ensuring that businesses and organizations comply with Vermont's tax laws, particularly when making exempt purchases or performing other tax-exempt activities. Whether it's proving tax-exempt status, registering a business, or reporting taxable income, having the right documentation is key to smooth operations and compliance with the law.

One similar document to the Vermont S-3 form is the California Resale Certificate. Both certificates enable buyers to purchase goods without paying sales tax, on the condition that the purchased items will be resold in the course of business. The primary purpose is to prevent the taxation of the same item multiple times in the supply chain. However, they are governed by the tax laws specific to their respective states, which outline the criteria for what constitutes a valid purchase for resale.

The Florida Annual Resale Certificate for Sales Tax shares similarities with the Vermont S-3 form, in that both are used by purchasers to buy items tax-free for the purpose of resale. Florida’s version, however, uniquely allows for an annual renewal, which means businesses do not need to issue a new certificate for each purchase, as long as the certificate remains valid. This feature can significantly reduce paperwork and streamline procurement for resale businesses.

New York’s ST-120, Resale Certificate, also functions analogously to Vermont's S-3 form by allowing businesses to avoid sales tax on purchases intended for resale. Like the Vermont form, New York requires specific details about the buyer and seller, and a declaration of the exemption reason. The nuanced differences lie in the state-specific tax codes and regulations that determine how exemptions are claimed and processed, reflecting local legislative approaches to sales tax.

The Texas Sales and Use Tax Resale Certificate is another document with a purpose similar to Vermont's S-3 form. This certificate allows Texas businesses to purchase goods without paying state sales tax, provided those goods are bought for resale. The Texas certificate places a significant emphasis on the requirement for purchasers to have a valid sales tax permit, highlighting the state's regulatory framework designed to ensure compliance and prevent tax evasion.

Similarly, the Multistate Tax Commission (MTC) Uniform Sales & Use Tax Exemption/Resale Certificate – Multijurisdiction form offers a broader approach, enabling businesses to conduct tax-exempt purchases for resale across multiple states. While the Vermont S-3 form is state-specific, the MTC’s version attempts to simplify the exempt purchasing process for businesses operating in various jurisdictions, showcasing an effort to streamline interstate commerce.

The Illinois Certificate of Resale, like the Vermont S-3 form, requires sellers to collect and maintain records that substantiate the tax-exempt nature of a sale. Both forms necessitate detailed information about the transaction and caution the buyer about the legal implications of misuse. These requirements reflect a shared commitment to maintaining integrity and accountability in tax-exempt transactions.

Oregon, being a state without a sales tax, does not have a direct counterpart to the Vermont S-3 form. However, Oregon businesses purchasing goods for resale in states with sales tax may use similar exemption certificates, showcasing the adaptability of businesses to navigate varying tax landscapes. This scenario underlines the importance of understanding and utilizing resale certificates for tax compliance across state lines.

Lastly, the Streamlined Sales and Use Tax Agreement (SSUTA) Certificate of Exemption represents a collaborative effort among states to simplify and modernize sales and use tax collection and administration. While the Vermont S-3 form is specific to Vermont, the SSUTA certificate is accepted by multiple states, reflecting an initiative towards efficiency and uniformity in tax-exempt transactions. This agreement facilitates easier management for businesses engaged in resale activities across participating states.

Filling out the Vermont S-3 form, which serves as a sales tax exemption certificate for purchases intended for resale or by exempt organizations, requires careful attention to detail. Here are several do's and don'ts to help guide you through this process:

Correctly filling out the Vermont S-3 form is essential for ensuring your organization's purchases are properly exempt from sales tax when eligible. By following these guidelines, you can avoid common pitfalls and ensure the form serves its intended purpose effectively.

Understanding the Vermont S 3 Form, a Sales Tax Exemption Certificate, is crucial for both sellers and qualifying organizations or individuals making exempt purchases. Here are key takeaways about correctly filling out and utilizing this form:

Proper understanding and application of the S 3 Form can significantly impact compliance with Vermont's tax laws, benefiting both buyers entitled to exemptions and sellers in conducting taxable transactions.

Su 451 Av - Local option sales tax collected on jet fuel sales should not be included on this form but remitted with other returns.

Taxable Supplies - Capital gains and other Vermont-sourced income received from different entities are reported, ensuring accurate state income allocation.