Fill Out a Valid Vermont Pt 172 S Form

Fill Out a Valid Vermont Pt 172 S Form

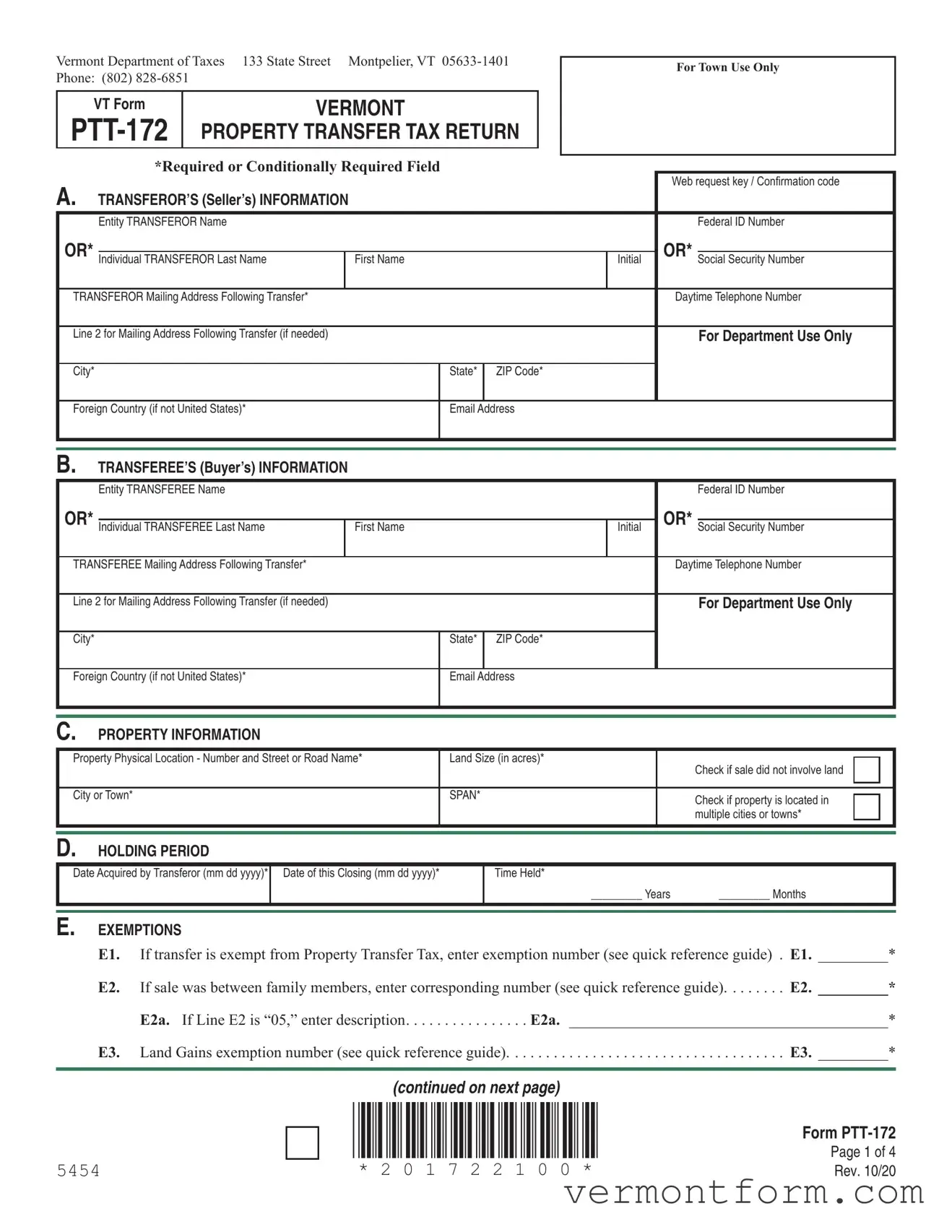

In the realm of property transactions in Vermont, the Vermont PT-172 S form stands as a critical document for capturing essential information about the transfer of property. At its core, this comprehensive form serves multiple functions: it collects details about both the seller (transferor) and the buyer (transferee), outlines specifics regarding the property in question, and records the financial aspects of the transaction, which includes tax calculations and exemptions. Additionally, it ensures compliance with local and state regulations by including sections on agricultural and managed forest land use, real estate withholding certification, and notifications related to local and state permits as well as Act 250 land use regulations. This form is not only a tax document but also a legal record that confirms the transference of property rights from one party to another. It requires mindfulness in providing accurate and complete information, from the parties' identification details to the intricacies of the property's description, its use before and after the transfer, the holding period, and any exemptions claimed. Such meticulous documentation underscores the importance of the Vermont PT-172 S form in the property transfer process, facilitating a smooth transition of ownership while adhering to statutory requirements.

Vermont Department of Taxes 133 State Street Montpelier, VT

VT Form |

VERMONT |

|

PROPERTY TRANSFER TAX RETURN |

For Town Use Only

|

|

*Required or Conditionally Required Field |

|

|

|

|

|

|

|

|

|||||

A. |

|

|

|

|

|

|

|

|

|

|

|

Web request key / Confirmation code |

|||

TRANSFEROR’S (Seller’s) INFORMATION |

|

|

|

|

|

|

|

|

|||||||

|

Entity TRANSFEROR Name |

|

|

|

|

|

|

|

|

|

|

Federal ID Number |

|||

OR* |

|

|

|

|

|

|

|

|

OR* |

|

|||||

Individual TRANSFEROR Last Name |

|

|

|

First Name |

|

|

Initial |

Social Security Number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

TRANSFEROR Mailing Address Following Transfer* |

|

|

|

|

Daytime Telephone Number |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

Line 2 for Mailing Address Following Transfer (if needed) |

|

|

|

|

|

For Department Use Only |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City* |

|

|

|

|

|

|

|

State* |

ZIP Code* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Foreign Country (if not United States)* |

|

|

|

|

|

Email Address |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B. |

TRANSFEREE’S (Buyer’s) INFORMATION |

|

|

|

|

|

|

|

|

||||||

|

Entity TRANSFEREE Name |

|

|

|

|

|

|

|

|

|

|

Federal ID Number |

|||

OR* |

|

|

|

|

|

|

|

|

|

OR* |

|

||||

Individual TRANSFEREE Last Name |

|

|

|

First Name |

|

|

Initial |

Social Security Number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

TRANSFEREE Mailing Address Following Transfer* |

|

|

|

|

Daytime Telephone Number |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Line 2 for Mailing Address Following Transfer (if needed) |

|

|

|

|

|

For Department Use Only |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City* |

|

|

|

|

|

|

|

State* |

ZIP Code* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Foreign Country (if not United States)* |

|

|

|

|

|

Email Address |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C. |

PROPERTY INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Property Physical Location - Number and Street or Road Name* |

|

Land Size (in acres)* |

|

Check if sale did not involve land |

|

|

|||||||||

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or Town* |

|

|

|

|

|

|

SPAN* |

|

|

|

Check if property is located in |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

multiple cities or towns* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D. |

HOLDING PERIOD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date Acquired by Transferor (mm dd yyyy)* |

Date of this Closing (mm dd yyyy)* |

|

Time Held* |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

_________ Years |

|

_________ Months |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E. |

EXEMPTIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E1. |

If transfer is exempt from Property Transfer Tax, enter exemption number (see quick reference guide) . E1. _________* |

|||||||||||||

|

E2. |

If sale was between family members, enter corresponding number (see quick reference guide). . . . . . . . E2. _________* |

|||||||||||||

|

|

E2a. If Line E2 is “05,” enter description |

E2a. _________________________________________* |

||||||||||||

|

E3. |

Land Gains exemption number (see quick reference guide). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E3. _________* |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

(continued on next page) |

|

|

|

|

|

||||

|

|

|

*201722100* |

|

|

|

Page 1 of 4 |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

||

5454 |

|

* 2 0 1 7 2 2 1 0 0 * |

|

|

|

Rev. 10/20 |

|||||||||

Transferee’s Name_____________________________________________________

Property Location _____________________________________________________

Date of this Closing____________________________________________________

*201722200*

* 2 0 1 7 2 2 2 0 0 *

F. |

TRANSFER INFORMATION |

|

|

|

|

|

||

|

F1. |

How did the Transferor acquire this property? (see quick reference guide) . . . . |

. . . . . . . . . . . . |

. . . . . . . . F1. _________* |

||||

|

|

F1a. |

If Line F1 is “04,” enter description |

F1a. _________________________________________* |

||||

|

F2. |

Interest conveyed in this transfer (see quick reference guide) . |

. . . . . . . . . . . . . |

. . . . . . . . . . . . |

. . . . . . . . F2. _________* |

|||

|

|

F2a. |

If Line F2 is “07,” enter percent of interest here |

. . . . . . . . . . . . . |

. F2a. ________________ . _______% * |

|||

|

|

F2b. |

If Line F2 is “08,” enter description |

F2b. _________________________________________* |

||||

|

F3. |

Type of building construction at time of transfer (see quick reference guide) . . |

. . F3. ________ ________ |

_______* |

||||

|

|

F3a. |

If Line F3 is “05,” enter number of units transferred . . . |

. . . . . . . . . . . . . |

. . . . . . . . . . . . |

. . . . . . . F3a. _________* |

||

|

|

F3b. |

If Line F3 is “06,” enter number of dwelling units transferred |

. . . . . . . . . . . . |

. . . . . . . F3b. _________* |

|||

|

|

F3c. |

If Line F3 is “20,” enter description |

F3c. _________________________________________* |

||||

|

F4. |

Was the transferee a tenant prior to this transfer? |

. . . . . . . . . . . . . . . |

. . . . . F4. |

cYes* |

cNo* |

||

|

F5. |

Financing |

F5. cConventional/Bank* |

cOwner Financing* |

cOther* |

|||

|

|

F5c. |

If Line F5 is “Other,” enter description |

F5c. _________________________________________* |

||||

|

F6. |

Do you intend to record this return with the Town/City within 60 days of the closing? . . F6. |

cYes* |

cNo* |

||||

|

|

|

|

|||||

G. |

AGRICULTURAL / MANAGED FOREST LAND USE VALUE PROGRAM, 32 V.S.A. CHAPTER 124 |

|

|

|||||

|

G1. |

Is all or part of the property being transferred enrolled in the Current Use |

|

cYes* |

cNo* |

|||

|

|

(Use Value Appraisal) Program? |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . |

G1. |

|||

|

G2. |

To continue enrollment in the Current Use Program, the new owner must submit a |

|

|

||||

|

|

Current Use Application within 30 days of the recording date. Will the new owner |

cYes* |

cNo* |

||||

|

|

be submitting that application? |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . |

. . . . . . . .G2. |

|||

|

|

|

|

|

|

|

||

H. |

TRANSFER INFORMATION |

|

|

|

|

|

||

|

H1. |

Transferor’s use of property BEFORE transfer (see quick reference guide) . . . |

. . . . . . . . . . . . |

. . . . . . . . H1. _________* |

||||

|

|

H1a. If Line H1 is “07,” “08,” or “09,” enter description. . . . |

H1a.__________________________________________* |

|||||

|

H2. |

Transferee’s use of property AFTER transfer (see quick reference guide) . . . . |

. . . . . . . . . . . . |

. . . . . . . . H2. _________* |

||||

|

|

H2a. If Line H2 is “07,” “08,” or “09,” enter description. . . . |

H2a.__________________________________________* |

|||||

|

H3. |

Was the property rented BEFORE transfer? |

. . . . . . . . . . . . . |

. . . . . . . .H3. |

cYes* |

cNo* |

||

|

H4. |

Will the property be rented AFTER transfer? |

. . . . . . . . . . . . . |

. . . . . . . .H4. |

cYes* |

cNo* |

||

|

H5. |

Have development rights been conveyed separately? |

. . . . . . . . . . . . . . . . . |

H5. |

cYes* |

cNo* |

||

|

H6. |

Does the transferee hold title to any adjoining property? |

. . . . . . . . . . . . . . |

. . . . . . . H6. |

cYes* |

cNo* |

||

|

H7. |

Is the transferee a grantor’s revocable trust? |

. . . . . . . . . . . . . |

H7. |

cYes* |

cNo* |

||

|

|

|

|

|

|

|

|

|

5454

(continued on next page)

For Town Use Only

Form

Page 2 of 4

Rev. 10/20

Transferee’s Name_____________________________________________________

Property Location _____________________________________________________

Date of this Closing____________________________________________________

*201722300*

* 2 0 1 7 2 2 3 0 0 *

I. |

REAL ESTATE WITHHOLDING CERTIFICATION |

|

|

|

||

|

I1. |

The transferee certifies that 2.5% VT Income tax has been withheld from the purchase |

|

|||

|

|

price and will be remitted to the Vermont Commissioner of Taxes with |

. . I1. cYes* |

cNo* |

||

|

|

Form |

||||

|

I2. |

If Line I1 is “No,” enter the withholding exemption number (see quick reference guide) |

I2. _________* |

|||

|

|

I2a. If Line I2 is “04,” enter Commissioner’s Certificate number |

I2a. ___________________________* |

|||

|

|

|

|

|

|

|

J. |

TAX CALCULATION |

|

|

|

|

|

Tax on Special Rate Property |

|

|

|

|

||

|

J1. |

Portion of value eligible for special principal |

|

|

|

|

|

|

residence rate (see instructions) . . . . |

. . . . J1. |

__________________________* |

|

|

|

J2. |

If transfer happened prior to July 1, 2011, |

|

|

|

|

|

|

enter the portion of value eligible for a |

|

|

|

|

|

|

special rate. (see instructions) |

. . . . J2. |

__________________________* |

|

|

|

J3. |

Total special rate value (Add Lines J1 & J2) . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

.J3. ___________________________* |

||

|

J4. |

Tax due on portion of value eligible for special rate |

|

|

||

|

|

(Multiply Line J3 by the tax rate of 0.005). . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

J4. ___________________________* |

||

|

J5. |

Only If Line E1 is “99”: |

|

|

|

|

|

|

Enter any portion of value in excess |

|

|

|

|

|

|

of $110,000 but below $200,000. . . . |

. . . J5. |

__________________________* |

|

|

|

J6. |

Tax due on exemption 99 for portion of value less than $200,000 |

|

|

||

|

|

(Multiply Line J5 by the tax rate of 0.0125 for exemption 99 only) |

.J6. ___________________________* |

|||

|

J7. |

Total due on portion of value eligible for special rates. (Add Lines J4 and J6) . . . |

.J7. ___________________________* |

|||

Tax on General Rate Property |

|

|

|

|

||

|

J8. |

Value paid or transferred as defined |

|

|

|

|

|

|

in 32 V.S.A. § 9601(6) |

J8. |

__________________________* |

|

|

|

J9. |

Value paid or transferred for personal |

|

|

|

|

|

|

property |

. . . J9. |

__________________________* |

|

|

|

J10. |

Value paid or transferred for real property |

|

|

|

|

|

|

(Subtract Line J9 from Line J8) . . |

. . . . J10. |

__________________________* |

|

|

|

J11. |

Enter amount from Line J3 above . . |

. . . J11. |

__________________________* |

|

|

|

J12. |

Enter amount from Line J5 above |

. . . . J12. |

__________________________* |

|

|

|

J13. |

Subtract Lines J11 and J12 from |

|

|

|

|

|

|

Line J10 |

J13. |

__________________________* |

|

|

|

J14. |

Tax due on portion of value subject to the General Rate (Multiply Line J13 |

|

|

||

|

|

by the tax rate of 0.0145 which includes a 0.002 surcharge for the Clean |

|

|

||

|

|

Water Fund, 32 V.S.A. § 9602a) . . |

. . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

J14. ___________________________* |

|

Total Tax Due |

|

|

|

|

|

|

|

J15. |

Total Tax Due (Add Lines J7 and J14) |

. . . . . . . . . . . . . . . . . . . . . . . . |

J15. ___________________________* |

||

|

|

|

|

|

|

|

5454

(continued on next page)

For Town Use Only

Form

Page 3 of 4

Rev. 10/20

Transferee’s Name_____________________________________________________

Property Location _____________________________________________________

Date of this Closing____________________________________________________

*201722400*

* 2 0 1 7 2 2 4 0 0 *

LOCAL AND STATE PERMITS AND ACT 250 NOTICE

This serves as notice that:

•The property being transferred may be subject to regulations governing potable water supplies and wastewater systems under 10 V.S.A. Chapter 64 and building, zoning and subdivision regulations;

•The property being transferred may be subject toAct 250 regulations regarding land use and development under 10 V.S.A. Chapter 151;

•The parties have an obligation to investigate and disclose knowledge regarding flood regulations affecting the property.

To determine if the property is in compliance with or exempt from these rules, contact the relevant agency. Contact information is provided in the instructions.

Transferor and Transferee state that the information submitted on this return is true, correct and complete to the best of their knowledge.

Prepared by (print or type) ____________________________________________ * |

|

Preparer’s Address _________________________________________________ * |

Preparer’s Email Address ______________________________________________ * |

__________________________________________________________________ |

Preparer’s Telephone __________________________________________________ * |

|

|

|

|

|

|

This section to be completed by Town or City Clerk

Book Number* |

Page Number* |

Grand List year* |

|

|

|

City or Town* |

Parcel ID Number |

Date of Record* |

|

|

|

Grand List Value |

Grand List Category* |

SPAN* |

|

|

|

Comments, additional information, etc. |

|

|

|

|

|

cDuplicate Return Suspected |

cPortion of the Property Sold |

cOriginal Return Waiting on Deed |

|

ACKNOWLEDGMENT |

|

Return received. |

|

|

SIGNED__________________________________________________________________ , Clerk |

DATE ______________________________________________ |

|

|

|

|

|

|

|

Town or City: Please forward the ORIGINAL form to the Vermont Department of Taxes within 30 days of receipt.

Do not redact the SSN/FEIN on the original.

* Please use the following numeric

Residential <6 Acres |

01 |

Residential >6 Acres |

02 |

Mobile Home/Un |

03 |

Mobile Home/La |

04 |

Seasonal <6 Acres |

05 |

5454

Seasonal >6 Acres |

06 |

Commercial |

07 |

Commercial Apt |

08 |

Industrial |

09 |

Utilities Elec |

10 |

For Town Use Only |

|

Utilities Other . . . . . . . . . . . . . . . 11

Farm . . . . . . . . . . . . . . . . . . . . . . 12

Other . . . . . . . . . . . . . . . . . . . . . . 13

Woodland . . . . . . . . . . . . . . . . . . 14

Miscellaneous . . . . . . . . . . . . . . . 15

Form

Page 4 of 4

Rev. 10/20

| Fact | Detail |

|---|---|

| Purpose | The form is used for reporting property transfers to the Vermont Department of Taxes. |

| Sections Included | Transferor and Transferee Information, Property Information, Exemptions, Transfer Information, Real Estate Withholding Certification, Tax Calculation, Local and State Permits, and Act 250 Notice. |

| Governing Law | 32 V.S.A. Chapter 124 for agricultural or managed forest land use value program and 10 V.S.A. Chapter 151 for Act 250 regulations on land development and use. |

| Key Features | Includes fields for detailed information on the property, the parties involved, and financial calculations related to the tax involved with the transfer. |

| Requirement for Submission | It must be filled out with true, correct, and complete information as known by the Transferor and Transferee and submitted to the Town or City Clerk, who then forwards it to the Vermont Department of Taxes. |

Filling out the Vermont PT-172 S form is a crucial step in the process of transferring property within the state. This document ensures that all necessary taxes related to the transfer are correctly calculated and paid. Below is a clear guide on how to complete the form properly. It's important to pay attention to detail and provide accurate information to avoid any delays or issues with the property transfer.

Following the step-by-step instructions above will streamline the process of accurately completing the Vermont PT-172 S form. Once finished, review the document to confirm all information is correct and complete before submission to the appropriate town or city clerk, alongside the original form being forwarded to the Vermont Department of Taxes within the specified timeframe.

What is the Vermont PT-172 S form used for?

The Vermont PT-172 S form, known as the Property Transfer Tax Return, is utilized during the sale or transfer of property within the state of Vermont. This document is required to report the sale to the Vermont Department of Taxes and is necessary to determine the property transfer tax owed by the seller (transferor) or buyer (transferee). The information captured on this form includes details about the transferor and transferee, property specifics, financial information relating to the transfer, and any applicable exemptions that might reduce the transfer tax obligation.

Who needs to complete the PT-172 S form?

Both the seller (transferor) and the buyer (transferee) of the property are responsible for ensuring the PT-172 S form is completed accurately and submitted to the Vermont Department of Taxes. The form requires information from both parties, including names, contact information, details about the property being transferred, the sale price, and any exemptions claimed to reduce the tax liability related to the transfer. It is often prepared by the legal or real estate professionals involved in the transaction on behalf of their clients.

Are there any exemptions to the property transfer tax that can be claimed on this form?

Yes, the PT-172 S form includes sections for claiming exemptions to the property transfer tax. These exemptions can significantly reduce the tax liability for the transfer. Some common exemptions include transfers between certain family members, transfers of property to government entities or non-profit organizations, and transfers where the property is enrolled in the Current Use Program. To claim an exemption, the appropriate exemption number from the provided quick reference guide must be entered on the form, and, in some cases, a detailed description of the exemption reason is required.

What happens if the PT-172 S form is not filed within the required timeframe?

Failing to file the PT-172 S form within the mandated timeframe can result in penalties and interest charges. The form is typically required to be submitted and the corresponding transfer tax paid at the time of the property transfer or shortly thereafter. Vermont law stipulates that the original form must be forwarded by the town or city clerk to the Vermont Department of Taxes within 30 days of the transfer. Buyers and sellers are encouraged to ensure prompt submission of the form by their legal or real estate representatives to avoid any late filing penalties and to ensure compliance with Vermont tax laws.

Filling out the Vermont PT-172 S form can be daunting, and mistakes are not uncommon. However, understanding and avoiding these common errors can streamline the process and ensure accuracy. Here is a breakdown of seven frequent mistakes:

By avoiding these mistakes, individuals can ensure a smoother, more accurate process when dealing with property transfer taxes in Vermont. Attention to detail and a careful review of the entire form before submission can prevent these common errors, leading to timely and successful processing of the Vermont PT-172 S form.

When dealing with property transfers in Vermont, specifically utilizing the Form PT-172 for property transfer tax returns, various additional forms and documents are often needed to ensure a smooth and compliant transaction. Here’s a list of some commonly used documents:

These documents play vital roles in the property transfer process, supporting and validating the information in the PT-172 form. They ensure legal compliance, provide essential details about the property and its history, secure the interests of both buyer and seller, and facilitate a transparent and lawful property transfer.

The Vermont PT-172 S form, required for property transfer tax returns within the state, shares similarities with various other documents commonly used in real estate transactions and tax reporting. Each of these documents plays a vital role in ensuring compliance with legal requirements, facilitating property transfers, or capturing essential information for taxation purposes.

One such document is the HUD-1 Settlement Statement, which, like the Vermont PT-172 S form, outlines the financial details of a property transaction. Both documents itemize charges, fees, and adjustments between buyers and sellers. However, the HUD-1 is more focused on the closing costs associated with mortgage transactions, providing a comprehensive breakdown of fees paid by both parties.

The Warranty Deed serves a different purpose but is related in the real estate transaction process. It guarantees that the seller holds clear title to the property and has the right to sell it, which subtly intersects with information on the Vermont PT-172 S form indicating the transferor’s and transferee’s details and the property's clear passage from one party to another.

The Grant Deed, similar to a Warranty Deed, transfers ownership from one person to another, ensuring the property has not been sold to someone else. Although it does not guarantee against all liens or debts as the Warranty Deed does, it operates in a related domain as the Vermont PT-172 S form by facilitating the transfer process, albeit with less focus on tax implications.

An Affidavit of Property Value, required in some jurisdictions, is filed with the county recorder's office alongside the deed. It includes details about the transfer that are also captured in the Vermont PT-172 S form, such as the property's sale price, which can be essential for tax assessment purposes.

IRS Form 1099-S is another document related to the transfer of real estate, specifically focusing on reporting the sale's proceeds to the Internal Revenue Service. While the Vermont PT-172 S form captures details relevant to state tax obligations, Form 1099-S addresses federal tax reporting requirements, showing the interconnectedness of property transfers and tax compliance at different government levels.

The Uniform Residential Loan Application is indirectly related to property transfer processes. While it focuses on the borrower's information to secure a mortgage, the details surrounding ownership transfer in the Vermont PT-172 S form also impact the mortgage process, making both documents essential at different stages of buying a property.

The Statement of Information, requested during the escrow process, is used to differentiate sellers and buyers from others with similar names. Although not directly related to tax, its role in clarifying the parties’ identities in a property transfer complements the information required in the Vermont PT-172 S form, such as the transferor's and transferee's names and addresses.

The Title Insurance Policy is a document ensuring the property buyer against losses from disputes over property ownership. While it offers protection after the transaction, similar to how the Vermont PT-172 S form captures details during the transaction, both are crucial for safeguarding interests in the realm of property transfers.

Finally, the Mortgage Agreement details the loan specifics agreed upon by the buyer and the lender. Its significance parallels the Vermont PT-172 S form since both are integral in the property buying process. The form documents the transfer and tax implications, while the mortgage agreement lays out the financing that often makes the transfer feasible.

The Real Estate Withholding Tax Statement, similar to the Vermont PT-172 S form, captures tax-related information pertinent to property transactions. Specific to certain states, it reports income from real estate sales to state tax authorities, highlighting the overlap in tax reporting obligations across different types of transactions.

When filling out the Vermont PT-172 S form, attention to detail and accuracy are crucial. Below are some tips to ensure a smooth and error-free submission:

Following these guidelines can help facilitate a hassle-free submission of the Vermont PT-172 S form.

One common misconception is that the Vermont Pt 172 S form is only for property sales between two individuals. In truth, the form accommodates both individual and entity transfers, requiring detailed information regarding the transferor(s) and transferee(s), including their entity name, Federal ID Number, or Social Security Number.

Many believe that this form is strictly for reporting the financial aspects of a property transfer, such as the sale price. However, it covers a wider array of information, including exemptions, property use before and after the transfer, whether the property was rented, and if development rights have been conveyed separately. This comprehensive approach ensures a thorough documentation process that extends beyond mere financial transactions.

It's a common misunderstanding that filling out the Vermont Pt 172 S form relieves parties from investigating and disclosing knowledge regarding flood regulations affecting the property. The form explicitly states the parties' obligation to investigate and disclose knowledge regarding flood regulations, emphasizing the need for due diligence in understanding how these regulations might impact the property being transferred.

Some assume that the section on Agricultural/Managed Forest Land Use Value Program is irrelevant if the property is not currently enrolled in the program. However, indicating whether the property is part of this program and if the new owner intends to continue enrollment is crucial. This information helps the state manage these special valuation programs and ensure compliance with their regulations.

Another misconception is that once the Vermont Pt 172 S form is completed and filed, no further action is required on the part of the transferor or transferee regarding the property's transfer tax obligations. In reality, the form includes sections such as the Real Estate Withholding Certification, which may require additional actions, like withholding Vermont income tax from the purchase price and remitting it with Form REW-171 within 30 days of the closing.

Lastly, there's a misunderstanding that all property transfers are subject to the same tax calculation process. The form differentiates between General Rate Property and Special Rate Property, each subject to different tax structures. Moreover, it accounts for exemptions and special circumstances that might affect tax calculations, highlighting the complexity and variability of property transfer taxes in Vermont.

When it comes to completing and utilizing the Vermont PTT-172 Property Transfer Tax Return, there are several key points you should keep in mind to ensure a smooth process. Understand these elements to avoid potential setbacks:

Accurately completing and promptly submitting the Vermont PTT-172 form is essential for any property transfer. It not only helps in correctly calculating and reporting taxes due but also in ensuring that all legal documents are in order for the ownership transfer. Paying close attention to the form's requirements can save you from potential legal and financial complications down the line.

Paper File - Completing this form is the first step in advocating for oneself in the legal system without the direct help of a lawyer.

What Is Eft in E Commerce - Key information about transitioning Vermont tax payments to an electronic format using ACH Credit, benefiting businesses with efficient processing.