Fill Out a Valid Vermont In 152 Form

Fill Out a Valid Vermont In 152 Form

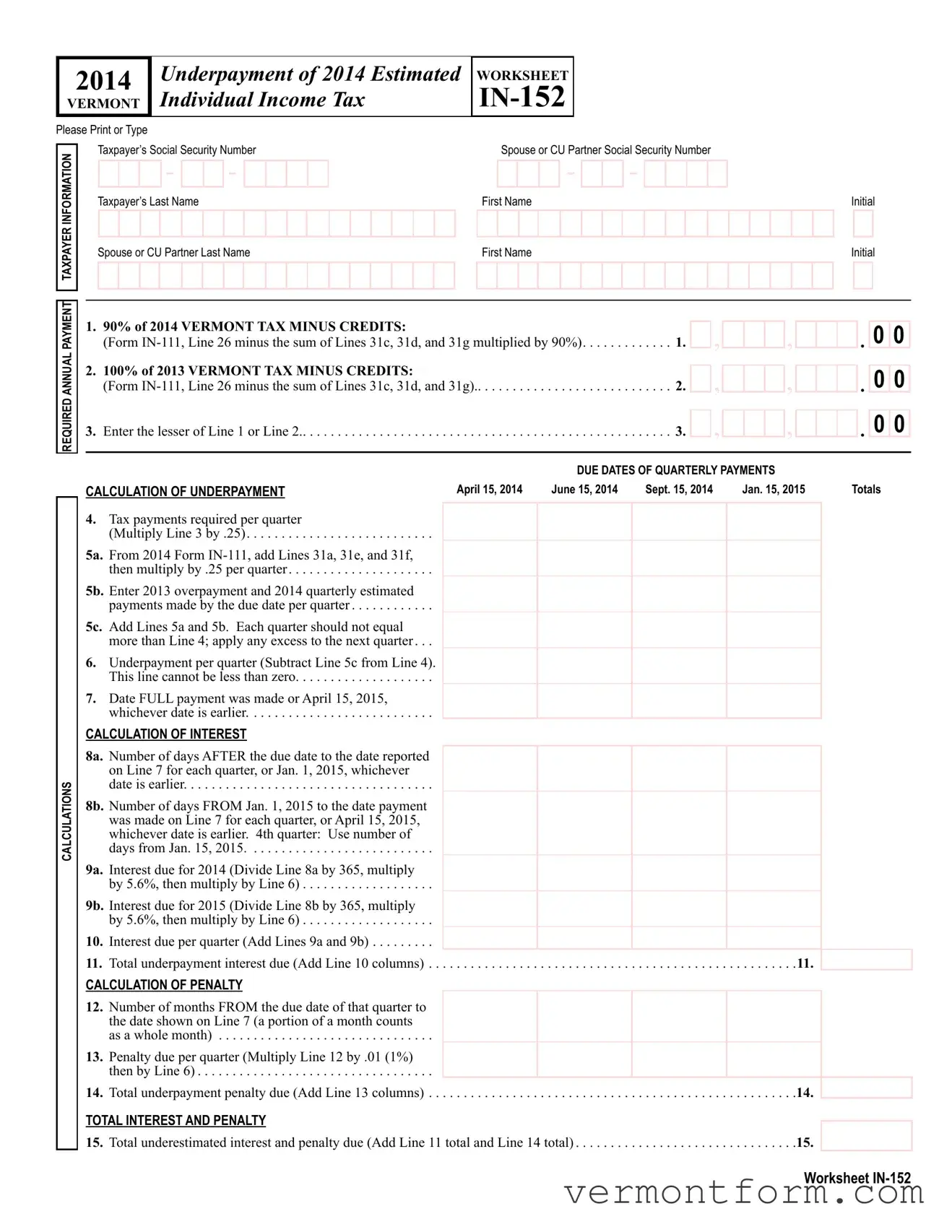

Navigating the complexities of individual income tax requirements can be a daunting task for Vermont residents, particularly when it comes to understanding the nuances of underpayment. The Vermont IN-152 form provides a structured approach for those who may not have adequately paid their estimated tax for the year 2014. It demands meticulous attention to detail, requiring taxpayers to first determine the required annual payment, which is intricately calculated based on 90% of the current year's tax minus credits or 100% of the previous year's tax minus credits, whichever is lesser. The form then guides taxpayers through scheduling their quarterly payments, calculating underpayments, and determining any accrued interest and penalties due to late or insufficient payments. These calculations take into account specific dates for both the due dates of quarterly payments and the full payment date to accurately assess any financial penalties. For individuals navigating the aftermath of underpayment, the Vermont IN-152 form serves as a critical tool, offering a step-by-step worksheet that not only helps in rectifying past payment oversights but also in understanding the impact of these actions on one's fiscal responsibilities.

|

2014 |

|

|

Underpayment of 2014 Estimated |

|||||||||||||||||

VERMONT |

|

Individual Income Tax |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Please Print or Type |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

Taxpayer’s Social Security Number |

||||||||||||||||||

INFORMATION |

|

|

|||||||||||||||||||

|

|

|

|

|

|

- |

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Taxpayer’s Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

TAXPAYER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse or CU Partner Last Name |

|||||||||||||||||||

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WORKSHEET

Spouse or CU Partner Social Security Number

|

|

|

|

- |

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

First Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REQUIRED ANNUAL PAYMENT

CALCULATIONS

1. |

90% OF 2014 VERMONT TAX MINUS CREDITS: |

|

|

|

|

|

, |

|

|

|

, |

|

|

|

. |

0 |

0 |

|

(Form |

. . . . 1. |

|

|

|

|

|

|

|

|

|||||||

2. |

100% OF 2013 VERMONT TAX MINUS CREDITS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

, |

|

|

|

. |

0 |

0 |

||

|

(Form |

. . . . . . . . . . . . . |

. . . . 2. |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

||||||||||

3. |

Enter the lesser of Line 1 or Line 2.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. |

|

|

, |

|

|

|

, |

|

|

|

. |

0 |

0 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DUE DATES OF QUARTERLY PAYMENTS |

|

|

|

|

|

|||||||||

CALCULATION OF UNDERPAYMENT |

April 15, 2014 |

June 15, 2014 |

Sept. 15, 2014 |

|

Jan. 15, 2015 |

|

Totals |

|

|||||||||

4.Tax payments required per quarter

|

(Multiply Line 3 by .25) |

______________________________________________________ |

5A. |

From 2014 Form |

|

|

then multiply by .25 per quarter |

______________________________________________________ |

5B. |

Enter 2013 overpayment and 2014 quarterly estimated |

|

|

payments made by the due date per quarter |

______________________________________________________ |

5C. |

Add Lines 5a and 5b. Each quarter should not equal |

|

|

more than Line 4; apply any excess to the next quarter. . . |

______________________________________________________ |

6.Underpayment per quarter (Subtract Line 5c from Line 4).

|

This line cannot be less than zero |

______________________________________________________ |

7. |

Date FULL payment was made or April 15, 2015, |

|

|

whichever date is earlier |

|

CALCULATION OF INTEREST |

|

|

8A. |

Number of days AFTER the due date to the date reported |

|

|

||

|

on Line 7 for each quarter, or Jan. 1, 2015, whichever |

|

|

date is earlier |

______________________________________________________ |

8B. |

Number of days FROM Jan. 1, 2015 to the date payment |

|

|

was made on Line 7 for each quarter, or April 15, 2015, |

|

|

whichever date is earlier. 4th quarter: Use number of |

|

|

days from Jan. 15, 2015 |

______________________________________________________ |

9A. |

Interest due for 2014 (Divide Line 8a by 365, multiply |

|

|

by 5.6%, then multiply by Line 6) |

______________________________________________________ |

9B. |

Interest due for 2015 (Divide Line 8b by 365, multiply |

|

|

by 5.6%, then multiply by Line 6) |

______________________________________________________ |

10. |

Interest due per quarter (Add Lines 9a and 9b) |

|

11. Total underpayment interest due (Add Line 10 columns) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11.

CALCULATION OF PENALTY

12.Number of months FROM the due date of that quarter to the date shown on Line 7 (a portion of a month counts

as a whole month) |

______________________________________________________ |

13. Penalty due per quarter (Multiply Line 12 by .01 (1%) |

|

then by Line 6) |

|

14. Total underpayment penalty due (Add Line 13 columns) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14.

TOTAL INTEREST AND PENALTY

15. Total underestimated interest and penalty due (Add Line 11 total and Line 14 total) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15.

Worksheet

| Fact | Detail |

|---|---|

| Purpose | Used to calculate underpayment of estimated tax and associated interest/penalties for Vermont individual income tax. |

| Components | Includes required annual payment calculations, due dates of quarterly payments, calculation of underpayment, calculation of interest, and calculation of penalty. |

| Governing Law | Vermont State Income Tax Laws. |

| Year Specific | Form is specific to the 2014 tax year, requirements based on 2013 tax filings. |

Filling out Vermont's IN-152 form accurately is essential for any individual who has underpaid their 2014 estimated state income tax. This form guides the taxpayer through calculating the underpayment amount, any resulting interest, and penalties due. Correct completion helps in resolving your tax responsibilities efficiently. Below are the outlined steps to fill out the form.

After completing these steps, the form IN-152 helps ensure accurate calculation and reporting of any underpayment of estimated tax, interest, and penalties. Review your calculations carefully and submit the form to the Vermont Department of Taxes to rectify your tax obligation for the year 2014.

What is the Vermont IN-152 form, and who needs to fill it out?

The Vermont IN-152 form is a document designed for individuals to calculate and report the underpayment of estimated tax for the year 2014. It is required for taxpayers who have not paid enough tax throughout the year through withholding or by making estimated tax payments. Individuals, including those with a spouse or Civil Union (CU) Partner, need to utilize this form if their payments fell below the required threshold calculated based on their income.

How do you determine if you underpaid your estimated tax for 2014?

To determine if there was an underpayment, you start with the "REQUIRED ANNUAL PAYMENT CALCULATIONS" section of the IN-152 form. You need to calculate 90% of your 2014 Vermont tax minus credits (Formula: Form IN-111, Line 26 minus the sum of Lines 31c, 31d, and 31g multiplied by 90%) and compare it with 100% of your 2013 Vermont tax minus credits. The lesser of these two figures is your required annual payment. If your actual payments made by the due dates are less than this required payment, you underpaid your estimated tax.

What are the due dates for quarterly payments, and how do you calculate the amount due each quarter?

The due dates for quarterly payments are April 15, June 15, September 15 of the tax year, and January 15 of the following year. To calculate the amount due each quarter, you must divide the required annual payment (the lesser value from Line 1 or Line 2 of the form) by four. This gives you the tax payments required per quarter. You must compare the actual payments made by these due dates, including overpayments from the prior year and any estimated payments made, to determine if there is an underpayment for any quarter.

How is the interest and penalty for underpayment calculated on the Vermont IN-152 form?

Interest on underpayment is calculated separately for 2014 and 2015. For both years, you divide the number of days after the due date until the payment was made (or until a specific cutoff date) by 365, then multiply by 5.6%, and then multiply that result by the amount of underpayment for each quarter. The penalty is calculated by multiplying the number of months (or portion thereof) from the due date of the quarter to the payment date by 1%, then by the underpayment amount for that quarter. Total underpayment interest for all quarters is summed up, as is the total penalty, to determine the overall interest and penalty due.

Filling out tax forms can be daunting, and it's easy to make mistakes. Here are seven common mistakes to avoid when filling out Vermont's Form IN-150, the Underpayment of Estimated Tax form:

Steering clear of these pitfalls will help ensure that the process of filling out Form IN-152 goes smoothly and accurately, minimizing the risk of incurring unnecessary penalties or delays.

When handling the Vermont IN-152 form, an individual is navigating the waters of estimated tax payments and the complexities associated with underpayments for a given tax year. This is not a journey typically made with a single document in hand. To effectively manage, calculate, and rectify underpayments, there are several other forms and documents that often accompany the Vermont IN-152 form. Each serves a specific purpose and aids in ensuring accuracy and compliance with state tax laws.

Navigating tax obligations efficiently requires a comprehensive approach, involving numerous documents and forms beyond the Vermont IN-152. By understanding and utilizing each relevant document, individuals can ensure that they remain compliant with tax laws while minimizing potential penalties and interest related to underpayments. Whether you're tackling this for the first time or need a refresher, keeping these forms at hand simplifies the process.

The Form 1040-ES, "Estimated Tax for Individuals," shares a core similarity with the Vermont IN-152 form in that they both are involved in calculating and paying estimated taxes. The Form 1040-ES is used by individuals to figure out and pay their estimated federal income tax for those who are not subject to withholding taxes, similar to how the IN-152 form is used at the state level for Vermont residents. Both forms help taxpayers avoid underpayment penalties by guiding them through the calculation of estimated tax payments that should be made quarterly.

The Form 2210, "Underpayment of Estimated Tax by Individuals, Estates, and Trusts," is another document that closely mirrors the Vermont IN-152 form. This form is used to determine whether an individual has paid enough tax through withholding or estimated tax payments and to calculate the penalty for underpayment if applicable. Like the IN-152, the Form 2210 is concerned with the underpayment of estimated tax, but it operates within the federal taxation framework. Both documents require a detailed calculation of payments due, underpayments, and applicable interests or penalties.

Another document that resembles the Vermont IN-152 form is the Schedule AI, "Annualized Income Installment Method," which is part of Form 2210. Schedule AI is specifically designed for taxpayers who do not receive their income evenly throughout the year and therefore can benefit from calculating their estimated tax payments based on the period income was actually earned. This schedule shares the IN-152's goal of accurately reflecting a taxpayer's payment obligations based on when income was received, thus potentially reducing or eliminating penalty for underpayment.

The VT Form IN-114, "Vermont Individual Income Tax Return," while primarily serving as the state's income tax return form, shares some functional similarities with the IN-152 in relation to tax payment and potential underpayment. Though its primary purpose is to report income and calculate the tax owed for the year, the final tax liability determined on Form IN-114 could indicate whether estimated payments made using IN-152 were sufficient, essentially complementing the IN-152's role in managing estimated tax payments throughout the year to avoid underpayment. Both forms cater to ensuring Vermont taxpayers meet their tax obligations accurately and on time, thereby interlinking their usability.

When it comes to handling your taxes, filling out forms accurately and timely is key to avoiding unnecessary penalties or interest. The Vermont IN-152 form, focused on the underpayment of estimated individual income tax, is one critical piece of this annual task. Here is a straightforward guide on the dos and don'ts when completing this form:

Things to Do:

Things Not to Do:

Completing the Vermont IN-152 form might seem daunting, but taking it step by step can simplify the process. By focusing on accurate and timely completion, you can fulfill your tax obligations without unnecessary stress or costs.

When it comes to understanding the Vermont IN-152 form, it's easy to encounter misconceptions. This form, critical for calculating underpayment of estimated individual income tax, often brings up questions and misunderstandings. Here are six common misconceptions about the Vermont IN-152 form:

Understanding the Vermont IN-152 form is crucial for correctly estimating and paying your individual income tax. By dispelling these common misconceptions, taxpayers can better navigate their tax responsibilities and avoid potential penalties.

When filling out and using the Vermont IN-152 form, it's vital to understand its purpose and how to accurately complete it. Here are seven key takeaways to guide you through this process:

In summary, the Vermont IN-152 form is essential for accurately calculating and reporting any underpayments of estimated taxes and associated interest and penalties. Careful attention to required payments, payment dates, and accurate record-keeping are pivotal in correctly filling out and using this form. Understanding these key takeaways can simplify the process and help avoid any unnecessary errors or penalties.

Taxable Supplies - Comprehensive reporting on the BI-472 influences the determination of state tax obligations for both resident and nonresident entities.

Vermont Nursing License - If renewing more than 30 days late, additional forms and verification of nursing practice are necessary—check the guidelines carefully.

Su 451 Av - Designed for aviation businesses, the Form SU-451-AV aids in reporting Sales and Use Tax on jet fuel in Vermont.