Fill Out a Valid Vermont Bi 472 Form

Fill Out a Valid Vermont Bi 472 Form

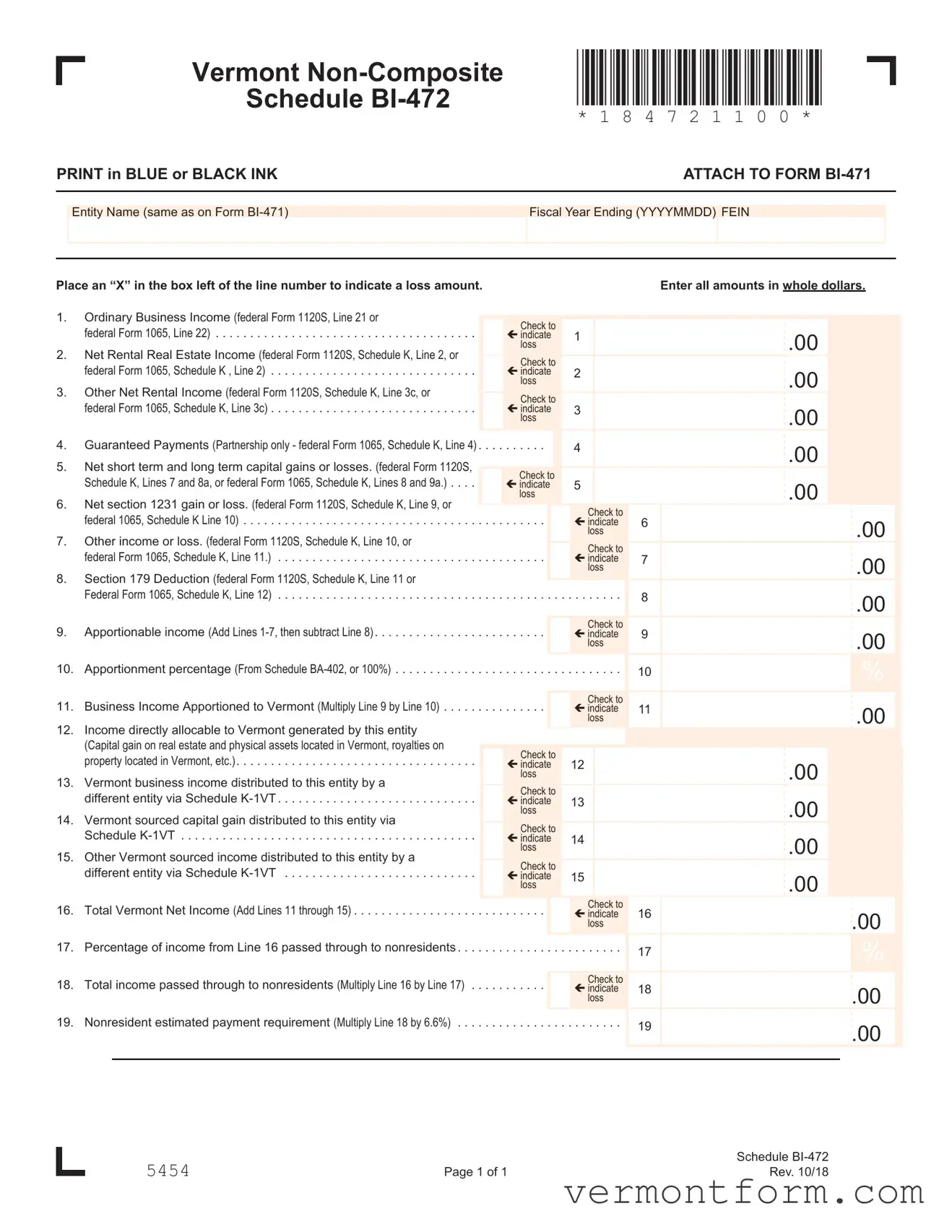

Navigating the complexities of Vermont's tax regulations requires a detailed understanding of specific forms and their applications, such as the Vermont BI-472 form. Designed for entities that must report non-composite financial activities, this form plays a crucial role in ensuring compliance with state taxation laws. By carefully filling out this form, businesses report various income types, such as ordinary business income, net rental real estate income, and other net income. It also requires entities to detail specific deductions and losses, including the Section 179 Deduction, to accurately calculate apportionable income. Moreover, the form serves as a means for determining the income that is directly apportioned to Vermont, including the apportionment percentage and Vermont-sourced income distributed through different entities. Entities use it to calculate Vermont net income, the percentage of income passed through to nonresidents, and subsequently, the total income passed to nonresidents. This meticulous documentation is essential for entities to meet their tax obligations and provides a framework for financial transparency within the state.

|

|

|

|

|

Vermont |

|

|

|

*184721100* |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

Schedule |

|

|

|

* 1 8 4 7 2 1 1 0 0 * |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

PRINT in BLUE or BLACK INK |

|

|

|

|

|

|

|

ATTACH TO FORM |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Entity Name (same as on Form |

|

Fiscal Year Ending (YYYYMMDD) |

FEIN |

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Place an “X” in the box left of the line number to indicate a loss amount. |

|

|

|

|

|

|

|

Enter all amounts in whole dollars. |

|

||||||||||||||

1. |

|

Ordinary Business Income (federal Form 1120S, Line 21 or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

federal Form 1065, Line 22) |

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

||||||||

2. |

|

Net Rental Real Estate Income (federal Form 1120S, Schedule K, Line 2, or |

|

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Check to |

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

federal Form 1065, Schedule K , Line 2) |

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||

3. |

|

Other Net Rental Income (federal Form 1120S, Schedule K, Line 3c, or |

|

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Check to |

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

federal Form 1065, Schedule K, Line 3c) |

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|

|

|

|

|

|||||

4. |

|

Guaranteed Payments (Partnership only - federal Form 1065, Schedule K, Line 4) |

4 |

|

|

.00 |

|

|

|

|

|

|

|

||||||||||

5. |

|

Net short term and long term capital gains or losses. (federal Form 1120S, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

Schedule K, Lines 7 and 8a, or federal Form 1065, Schedule K, Lines 8 and 9a.). . . |

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

||||||||

6. |

|

Net section 1231 gain or loss. (federal Form 1120S, Schedule K, Line 9, or |

|

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

Check to |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

federal 1065, Schedule K Line 10) |

|

6 |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

||||||||||||||

7. |

|

Other income or loss. (federal Form 1120S, Schedule K, Line 10, or |

|

|

|

loss |

|

|

|

|

|

|

|||||||||||

|

|

|

|

Check to |

7 |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

federal Form 1065, Schedule K, Line 11.) |

|

ç indicate |

|

|

.00 |

|

|

|||||||||||||

8. |

|

Section 179 Deduction (federal Form 1120S, Schedule K, Line 11 or |

|

|

|

loss |

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

Federal Form 1065, Schedule K, Line 12) |

8 |

|

|

.00 |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

9. |

|

Apportionable income (Add Lines |

|

Check to |

9 |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

ç indicate |

|

|

.00 |

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|||||||

10. |

Apportionment percentage (From Schedule |

10 |

|

|

|

|

% |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

11. |

Business Income Apportioned to Vermont (Multiply Line 9 by Line 10) |

|

Check to |

11 |

|

|

|

|

|

|

|

|

|

||||||||||

|

ç indicate |

|

|

.00 |

|

|

|||||||||||||||||

12. |

Income directly allocable to Vermont generated by this entity |

|

|

|

loss |

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

(Capital gain on real estate and physical assets located in Vermont, royalties on |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

property located in Vermont, etc.) |

|

Check to |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

13. |

Vermont business income distributed to this entity by a |

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

different entity via Schedule |

|

13 |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

14. |

Vermont sourced capital gain distributed to this entity via |

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

Schedule |

|

14 |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

15. |

Other Vermont sourced income distributed to this entity by a |

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

different entity via Schedule |

|

15 |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

loss |

Check to |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

16. |

Total Vermont Net Income (Add Lines 11 through 15) |

|

16 |

|

|

|

|

|

|

|

|

|

|||||||||||

|

ç indicate |

|

|

.00 |

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|

||||||

17. |

Percentage of income from Line 16 passed through to nonresidents |

|

17 |

|

|

|

|

% |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

18. |

Total income passed through to nonresidents (Multiply Line 16 by Line 17) |

|

Check to |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

ç indicate |

18 |

|

|

.00 |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|

||||||

19. |

Nonresident estimated payment requirement (Multiply Line 18 by 6.6%) |

|

19 |

|

|

.00 |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5454 |

|

Schedule |

Page 1 of 1 |

Rev. 10/18 |

| Fact | Detail |

|---|---|

| Form Title | Vermont Non-Composite Schedule BI-472 |

| Ink Color for Filling Out | Must be filled out in blue or black ink |

| Attachment Requirement | Needs to be attached to Form BI-471 |

| Entity Information | Requires the same entity name as on Form BI-471 and includes sections for the fiscal year ending (YYYYMMDD) and FEIN |

| Loss Indication | Provides boxes to indicate loss amounts next to relevant line numbers |

| Income and Deductions Reporting | Covers various income types, losses, and the Section 179 Deduction, relating them to federal forms like Form 1120S and Form 1065 |

| Calculation of Vermont Net Income | Details the steps to calculate Vermont business income, including apportioned income and income directly allocable to Vermont |

| Governing Law | Vermont tax laws and regulations, particularly regarding nonresident income and business income apportionment |

Once you've gathered all the necessary documents for your fiscal responsibilities in Vermont, one of the key forms you might need to tackle is the Vermont Bi 472 form. This form is essential for accurately reporting various income types and deductions. It requires careful attention to detail and precise information from your financial records. Let's break down the process into manageable steps to ensure you fill out the form correctly and efficiently.

By following these steps, you'll be navigating the requirements of the Vermont Bi 472 form with confidence. Diligence in completing this form ensures compliance with Vermont tax laws and contributes to the smooth operation of your business’s financial obligations.

What is the Vermont BI-472 form used for?

The Vermont BI-472 form, known as the Non-Composite Schedule, serves a critical role in the state's tax system. It is designed for entities that operate within Vermont, allowing them to report various types of income, deductions, and the income distribution to their members or partners. Specifically, this form captures ordinary business income, net rental real estate income, other net rental income, guaranteed payments to partners, net capital gains or losses, net section 1231 gain or loss, other income or losses, and the Section 179 Deduction. Furthermore, it calculates apportionable income, details the apportionment percentage, and delineates business income apportioned to Vermont, including directly allocable income and Vermont-sourced income distributed through Schedule K-1VT. Finally, it also addresses the income passed through to nonresidents and the corresponding estimated payment requirements.

Who is required to fill out the Vermont BI-472 form?

Entities that are required to file Form BI-471, which includes corporations, partnerships, and other businesses operating in Vermont and deriving income from various sources within the state, must complete the BI-472 form. This requirement is not limited to entities based in Vermont but extends to any entity generating income within the state. The form is used to apportion and allocate business income according to Vermont tax laws, making its completion crucial for accurate state income tax reporting and compliance.

How does an entity fill out the Vermont BI-472 form?

Filling out the Vermont BI-472 form requires careful attention to the details of an entity's income and operations over the fiscal year. Entities must first report their ordinary business income, net rental income, and other specific types of income in whole dollars, marking a box to indicate any losses. They then calculate their apportionable income and determine their apportionment percentage, which may be 100% or derived from Schedule BA-402. This percentage is applied to find the business income apportioned to Vermont. Additionally, the form asks for details on Vermont-sourced income, such as capital gains on real property or income distributed by another entity via Schedule K-1VT. Entities must use information from their federal tax returns as a basis for these calculations, specifically referring to federal forms 1120S and 1065. Finally, the total Vermont net income and the income passed through to nonresidents are calculated, including the nonresident estimated payment requirement based on these figures.

Are there any specific color requirements for ink when filling out the Vermont BI-472 form?

Yes, when completing the Vermont BI-472 form, it is mandated that entities use either blue or black ink. This requirement ensures that the form is legible and that scanned or photocopied versions maintain their clarity for processing and review. Using the specified ink colors helps avoid processing delays or issues related to the readability of the information provided.

What happens if an entity doesn't fill out the Vermont BI-472 form?

Failure to complete and submit the Vermont BI-472 form can lead to several adverse consequences for the entity. Primarily, this failure could result in noncompliance with Vermont tax laws, potentially attracting penalties, fines, and interest on unpaid taxes. Additionally, it could delay the processing of the entity's tax filings, disrupt the accurate assessment of tax liabilities, and affect income distribution reporting for members or partners. Entities at risk of not meeting the submission deadline should seek guidance or assistance promptly to avoid these complications and ensure full compliance with state tax obligations.

Failing to Use the Correct Ink Color: The instructions clearly require that the form should be filled out in blue or black ink. Using different ink colors can lead to processing delays or even the rejection of the form because scanning machines are calibrated to recognize these specific colors.

Incorrect Entity Name Information: The entity name listed on the BI-472 form must match exactly as it appears on Form BI-471. Discrepancies between the forms can cause confusion, delay the processing of the document, and potentially lead to improperly assessed taxes.

Misunderstanding Date Formats: The Fiscal Year Ending date must follow the YYYYMMDD format. Incorrect formatting or unclear handwriting can lead to processing errors, as the exact end of the fiscal year is critical for accurate tax calculation.

Omitting the FEIN: The Federal Employer Identification Number (FEIN) is often overlooked. It is crucial for the identification of the entity within federal and state tax systems. Failing to provide this number can halt the processing of the form until the oversight is corrected.

Not Indicating Loss Amounts Correctly: If reporting a loss, an “X” must be placed in the box left of the line number. This step is frequently missed, leading to incorrect calculations of income or loss. It is important to be attentive to these indications to ensure the form reflects the financial reality of the entity accurately.

Mathematical Errors in Calculations: Errors in the addition, subtraction, or multiplication of figures, especially in determining the apportionable income and the apportionment percentage, are common. These mistakes can significantly affect the final tax liability. Double-checking all mathematical calculations before submitting the form can prevent such errors.

Incomplete Reporting of Income Types: Each line of the form requires a thorough examination of the different income types and deductions. Often, entities might skip sections that apply to them, like net rental income, capital gains, or Section 179 deductions. This oversight can lead to underreported income and the possibility of penalties.

In summary, while completing the Vermont BI-472 form may seem straightforward, attention to detail is paramount. Overlooking simple instructions, like ink color, or more complex aspects, such as accurately reporting and calculating different income types, can have significant ramifications. To ensure compliance and accuracy, a thorough review of the form and all applicable instructions before submission is advisable.

In the realm of business and taxation in Vermont, understanding and preparing the correct documentation is crucial for compliance and optimal financial health. The Vermont BI-472 form, known for its role in capturing non-composite business income information, stands as a pivotal piece in the tax filing puzzle for entities operating within the state. However, it rarely acts alone in the tax preparation process. Several other forms and documents often accompany the Vermont BI-472 form, each serving its unique purpose in the broader context of tax filing and business reporting.

Each of these forms and documents plays a specific role in ensuring that businesses comply with Vermont's tax laws and accurately report their income. From detailing the overall business income to apportioning income correctly between states, these documents collectively create a comprehensive view of an entity's financial and tax situation. Proper completion and submission of these documents, alongside the Vermont BI-472 form, ensure that businesses meet their obligations while potentially optimizing their tax outcomes.

The Vermont Schedule BI-472 form has similarities with the federal Form 1120S, U.S. Income Tax Return for an S Corporation. Both documents are designed to report income, deductions, and other financial information for businesses structured as S corporations. The BI-472 form references specific lines from Form 1120S, indicating that information from the federal return is necessary for completing the state-specific schedule. For instance, ordinary business income and net rental real estate income on the BI-472 are directly taken from lines on the Form 1120S.

Form 1065, U.S. Return of Partnership Income, is another document comparable to the Vermont BI-472. Designed for partnerships, Form 1065 collects information on the partnership's income, gains, losses, deductions, and credits. The BI-472 form requests details from specific lines of Form 1065 for items like guaranteed payments and other net rental income, demonstrating how these forms work together to ensure the accurate reporting of business income for multi-state operations.

The Schedule K-1 (Form 1065), Partner's Share of Income, Deductions, Credits, etc., is closely aligned with the BI-472 in that it provides detailed breakdowns of income sources and allocations for individual partners. With references to Schedule K-1 information for determining Vermont-sourced income distributed to the entity, the BI-472 leverages data from this federal form to calculate state-specific income attributions and obligations.

Schedule K of both Form 1120S and Form 1065 outlines the share of income, deductions, and credits for S corporations and partnerships respectively. The BI-472 form often looks at specific lines within Schedule K to determine the proper values for items like net rental income, capital gains or losses, and Section 179 deductions, demonstrating its reliance on the detailed breakdowns these schedules provide for state tax calculation purposes.

The Schedule BA-402, Apportionment & Allocation Schedule, is unique to Vermont and works in tandem with the BI-472. It assists in determining the apportionment percentage for multi-state businesses, a critical factor in calculating the portion of business income apportioned to Vermont. This form complements the BI-472 by providing a key piece of data necessary for completing the state income calculation.

Form 1120, U.S. Corporation Income Tax Return, though primarily for C corporations, shares common elements with the BI-472 in terms of reporting income, deductions, and credits. While the BI-472 form is more closely related to S corporations and partnerships, the overall structure and purpose of providing a comprehensive account of a business’s financial activities connect these documents.

The Schedule L (Form 1120), Balance Sheets per Books, while not directly referenced in the BI-472, is a federal form that parallels the need for detailed financial disclosures found in the BI-472. Businesses may use information from their balance sheets to support figures entered in the BI-472, highlighting the interconnected nature of these financial documents.

The Schedule M-1, Reconciliation of Income (Loss) per Books With Income per Return, serves a related purpose to adjustments made on the BI-472. It reconciles book income with taxable income, a process that may be necessary when filling out the Vermont form to account for differences in federal and state taxable income calculations.

Form 8825, Rental Real Estate Income and Expenses of a Partnership or an S Corporation, is akin to the BI-472 in that it details rental income and expenses which must be reported on both federal and state levels. Information from Form 8825 can directly impact values entered in the BI-472, especially regarding net rental real estate income and other rental income.

Finally, the Schedule K-1 (Form 1120S), Shareholder's Share of Income, Credits, Deductions, etc., mirrors the partnership version but for S corporations, providing a breakdown of income and deductions for shareholders. This document is essential for completing the BI-472 when the entity is an S corporation, ensuring that Vermont-sourced income is properly reported and taxed.

Filling out the Vermont BI-472 form accurately is crucial for reporting non-composite income to the state's tax department. To ensure that you complete this form correctly and avoid common mistakes, here are things you should and shouldn't do:

Things You Should Do:When discussing the Vermont BI-472 form, several misconceptions often arise. Clarifying these can help in understanding the form's purpose and how to accurately complete it.

Only for large businesses: There's a common belief that the Vermont BI-472 form is only for large entities. However, it's aimed at all entities that are subject to income through business operations in Vermont, regardless of their size.

Paper filing only: Another misconception is that this form must be filed in paper format. The reality is that entities can also file this form electronically, offering convenience and faster processing.

Only for profits: Some think that only entities with profits need to complete the BI-472. This form also requires reporting losses, as indicated by placing an "X" in the box left of the line number to signal a loss amount.

No need to report zero amounts: It's incorrectly assumed at times that zero amounts or non-operating incomes do not need to be reported. Every dollar, including zeros, should be accurately reported in whole numbers, as the form stipulates.

For individual tax reporting: The BI-472 form may be mistaken as a form for individual tax reporting. It's specifically designed for entities such as partnerships or S corporations to report their income, deductions, and credits related to business activity in Vermont.

Information only from federal returns is needed: While much of the information does come from federal forms (1120S or 1065), the BI-472 requires specific calculations and apportionments unique to Vermont tax law.

Only the current year's data is relevant: This form does focus on the current fiscal year's data, but certain situations may require referencing past years for accuracy, especially when dealing with losses or deductions that carry over.

Doesn't impact other state filings: Completing the BI-472 accurately can affect filings in other states, especially for entities operating across state lines, due to state-to-state variations in income apportionment and tax credit eligibility.

No penalties for late filing: Lastly, there's a misconception that late filing of the BI-472 form doesn't result in penalties. Late or inaccurate filings can lead to penalties and interest charges, just like with other tax forms.

Understanding these misconceptions and clarifying the actual requirements and purposes of the Vermont BI-472 form can lead to more accurate and compliant filings, benefiting entities operating within the state.

Filling out and using the Vermont BI-472 form, crucial for entities to correctly report income and calculate taxes owed to the state, involves meticulous attention to detail and a deep understanding of your entity’s financial activities. To ensure accuracy and compliance with Vermont tax laws, here are seven key takeaways that businesses should keep in mind:

Use the correct ink: It’s essential to print the form in blue or black ink, as specified, to ensure that the document is legible and accepted by the tax authorities.

Consistent entity naming: The entity name entered on the BI-472 form must match exactly with what is on Form BI-471, ensuring consistency across documents.

Reporting in whole dollars: When entering amounts, round to the nearest dollar and avoid including cents. This standardization helps in simplifying the calculation process.

Indicating losses correctly: An "X" should be placed in the box left of the line number to accurately indicate a loss, which is critical for the correct calculation of taxable income.

Understanding source documents: Information from federal forms such as 1120S (for S corporations) and 1065 (for partnerships) is pivotal. Knowledge of where to find corresponding figures on these federal forms is necessary for accurate reporting.

Calculating apportionable income: To arrive at the apportionable income, add lines 1 through 7 and then subtract line 8. This step is the basis for determining the amount of income attributable to Vermont.

Meeting nonresident obligations: For businesses with nonresident members, calculating the income passed through to these members and the corresponding estimated payment requirement is crucial for compliance.

By closely following these guidelines, entities can effectively fill out and use the Vermont BI-472 form to accurately report their income, ensuring compliance with state tax laws and avoiding potential penalties for errors or omissions. Always keep updated with any changes to tax forms or regulations to maintain compliance.

Business Tax Due Date 2023 - Preparation for submitting the S 1 Vermont form includes gathering necessary business details, such as trade names and NAICS codes.

Su 451 Av - A due date for the return ensures businesses stay on track with their tax obligations and avoid late penalties.

Vt Sales Tax Rate - Addresses the use of the certificate for both recurring and one-time purchases.