Fill Out a Valid Su 451 Av Form

Fill Out a Valid Su 451 Av Form

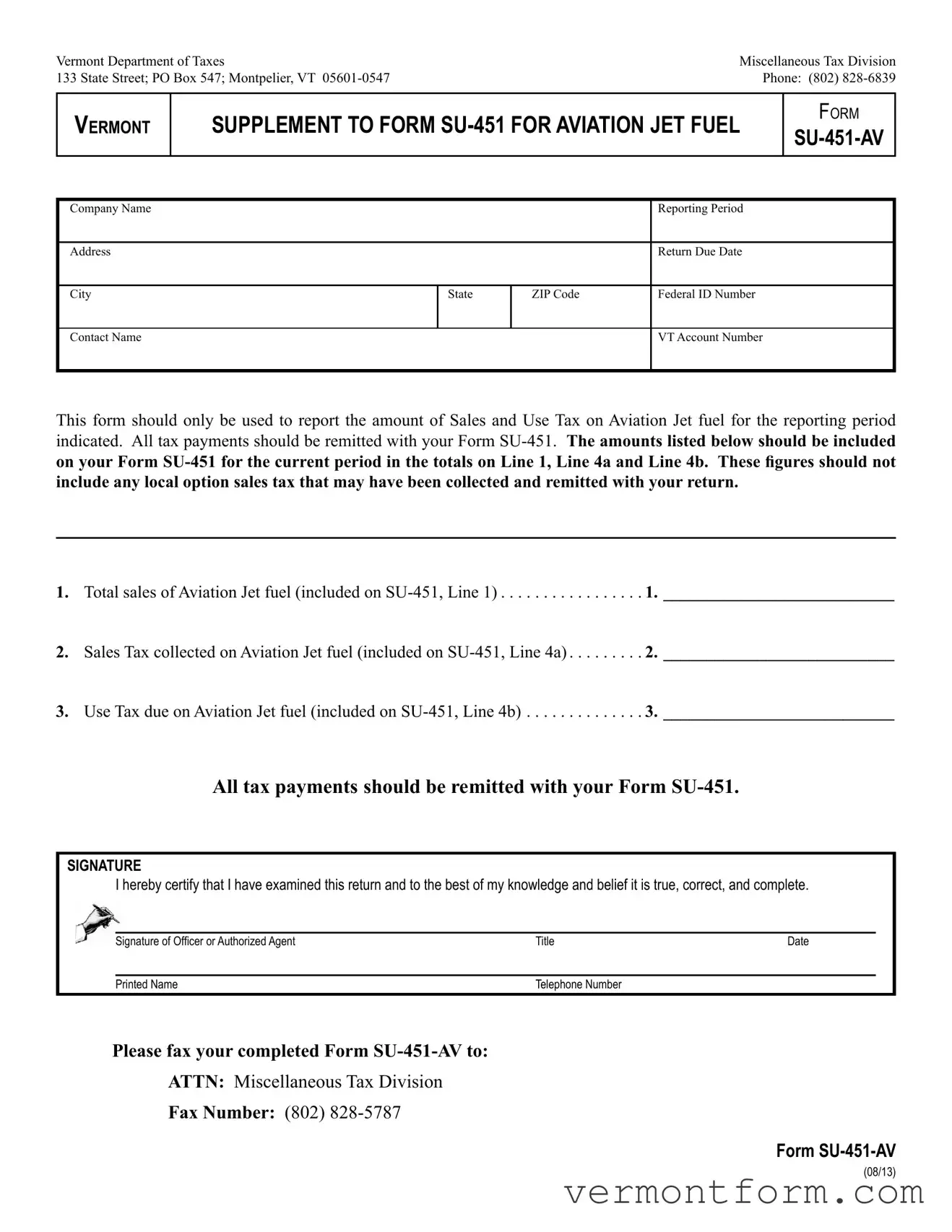

Navigating the complexities of tax reporting for aviation jet fuel in Vermont is streamlined with the introduction of the Supplement to Form SU-451, specifically designed for the aviation sector. Known as Form SU-451-AV, this document is an essential tool for companies operating within this niche, facilitating accurate Sales and Use Tax reporting relevant to their operations. The Vermont Department of Taxes has meticulously outlined the requirements for reporting and remitting taxes on aviation jet fuel sales and use, ensuring that all necessary financial activities are properly accounted for within the specified reporting period. Key elements of the form include the total sales of aviation jet fuel that are to be reported, alongside the sales tax collected and any use tax due, with clear instructions to exclude local option sales taxes from these figures. This form acts not only as a supplement but also as a critical part of the tax documentation, requiring the merging of these figures into the main Form SU-451 for a comprehensive tax return. The document underscores the importance of precision and compliance in financial reporting, necessitating the submission of accurate and correct information by an authorized officer or agent of the company. The streamlined process facilitated by Form SU-451-AV exemplifies Vermont's commitment to efficient tax administration within specialized sectors, highlighting the state's effort to accommodate the unique needs of the aviation industry.

Vermont Department of Taxes |

Miscellaneous Tax Division |

133 State Street; PO Box 547; Montpelier, VT |

Phone: (802) |

VERMONT

SUPPLEMENT TO FORM

FORM

Company Name

Reporting Period

Address

Return Due Date

City

State

ZIP Code

Federal ID Number

Contact Name

VT Account Number

This form should only be used to report the amount of Sales and Use Tax on Aviation Jet fuel for the reporting period

indicated. All tax payments should be remitted with your Form

include any local option sales tax that may have been collected and remitted with your return.

1.Total sales of Aviation Jet fuel (included on

2.Sales Tax collected on Aviation Jet fuel (included on

3.Use Tax due on Aviation Jet fuel (included on

All tax payments should be remitted with your Form

SIGNATURE

I hereby certify that I have examined this return and to the best of my knowledge and belief it is true, correct, and complete.

Signature of Oficer or Authorized Agent |

Title |

Date |

Printed Name |

Telephone Number |

|

Please fax your completed Form

ATTN: Miscellaneous Tax Division

Fax Number: (802)

FORM

(08/13)

| Fact | Detail |

|---|---|

| Form Purpose | It is used specifically to report the Sales and Use Tax on Aviation Jet Fuel. |

| Associated Primary Form | All reported amounts on the SU-451-AV need to be included in Form SU-451. |

| Exclusion | Local option sales tax is not to be included in the amounts reported. |

| Reportable Items | Includes total sales, sales tax collected, and use tax due on Aviation Jet Fuel. |

| Submission Information | The form should be faxed to the Miscellaneous Tax Division at the provided fax number. |

| Location | Vermont Department of Taxes, with a specific focus on the Miscellaneous Tax Division. |

| Governing Law | Subject to Vermont state tax regulations regarding the reporting and remittance of sales and use tax. |

Filling out the Form SU-451-AV can seem like a daunting task, but breaking it down into manageable steps can make the process smoother and ensure your tax reporting is accurate and complete. This form is crucial for companies in the aviation industry, particularly those dealing with aviation jet fuel sales and use tax. Once you have gathered all the necessary information, follow the step-by-step instructions below to complete your form correctly.

After completing the form, double-check all entered information for accuracy. Once you're confident everything is correct, fax your completed Form SU-451-AV to the Miscellaneous Tax Division using the fax number provided on the form. By following these detailed steps, companies can efficiently report their aviation jet fuel taxes, ensuring they remain compliant and avoid potential issues with tax filings.

Frequently Asked Questions about the SU-451-AV Form

The SU-451-AV form is a supplementary document specifically designated for reporting Sales and Use Tax on Aviation Jet Fuel in Vermont. Businesses dealing with aviation jet fuel use this form to accurately report the amount of tax collected or due for their sales and use of aviation jet fuel within the reporting period. This form complements the primary Form SU-451 by providing detailed figures that are necessary for the tax calculation.

The due date for submitting the SU-451-AV form coincides with the due date of your Form SU-451. The specific return due date is determined by the reporting period for which you are filing. It is imperative to submit the SU-451-AV alongside the SU-451 to ensure timely processing and to avoid potential late fees or penalties associated with late submissions.

Upon completion, the SU-451-AV form should be faxed to the Vermont Department of Taxes at the Miscellaneous Tax Division. The fax number for submission is (802) 828-5787. Ensure that the form is complete and the information provided is accurate before faxing it to the designated number to prevent any delays in processing.

The SU-451-AV form requires detailed information concerning the sales and use of aviation jet fuel. In particular, you will need to include:

Filling out government tax forms accurately is crucial to avoid errors that can lead to audits, fines, or other penalties. When it comes to the Vermont Department of Taxes Form SU-451-AV for reporting Sales and Use Tax on Aviation Jet Fuel, individuals often make several common mistakes. Identifying these errors can help ensure the process is completed correctly.

Not using the correct form version: The form is periodically updated by the Vermont Department of Taxes. Individuals sometimes use an outdated version of the form which may not have the current tax rates or requirements, leading to incorrect reporting.

Omitting the federal ID number: The federal ID number is critical for tax identification purposes. Failure to include this number can result in the submission being rejected or not properly processed.

Incorrect totals on designated lines: Lines 1, 4a, and 4b on the SU-451 AV form are specific for reporting total sales, sales tax collected, and use tax due on Aviation Jet Fuel, respectively. Errors in entering amounts on these lines can lead to underpayment or overpayment of taxes.

Forgetting to include local option sales tax details: While the SU-451 AV form specifically instructs not to include local option sales tax in the figures, taxpayers sometimes mistakenly include these amounts. This can distort the reported figures and complicate tax processing.

Misplacing the reporting period: The reporting period indicated at the top of the form must match the period for which the taxes are being reported. Entering the wrong reporting period can lead to discrepancies and potential issues with tax filings.

Failure to sign and date the form: An unsigned or undated form is considered incomplete and will not be processed. The signature certifies the accuracy of the information provided.

By avoiding these mistakes, individuals can streamline their tax filing process and ensure they are in compliance with Vermont's tax requirements for Aviation Jet Fuel.

The Vermont Department of Taxes leverages a variety of forms and documents to ensure comprehensive tax reporting and compliance, especially in specialized sectors like aviation. The Form SU-451-AV is a pivotal document for entities dealing with aviation jet fuel, necessitating the completion of various supplementary documents to ensure accurate tax filing and regulation adherence. Highlighted below are eight additional forms and documents that are commonly utilized alongside the SU-451-AV form to facilitate seamless tax operations within the aviation fuel sector.

Together, these forms build a framework for thorough and compliant tax practices within the aviation sector in Vermont. By utilizing the appropriate documents for various transactions and operations, businesses ensure adherence to both state and federal tax obligations, promoting transparency and fiscal responsibility. Understanding the purpose and requirement of each document is crucial in navigating the intricate landscape of tax reporting and compliance.

The Form 1040, used by the United States Internal Revenue Service for individual income tax returns, is similar to the SU-451-AV in its purpose of reporting and calculating taxes due. Both forms serve as a bridge between taxpayers and government entities, detailing the amount of tax owed for specific activities or income sources. Whereas the SU-451-AV focuses on the sales and use tax specifically for aviation jet fuel in Vermont, the Form 1040 encompasses a broader spectrum of income sources, deductions, and credits for individuals, highlighting the specialization of tax forms based on the nature of the tax obligation.

Another document that shares a resemblance with the SU-451-AV is the Form W-2, which employers use to report an employee's annual wages and the amount of taxes withheld from their paycheck. Both forms play crucial roles in tax administration, ensuring that the correct amount of tax is reported and paid to the government. While the SU-451-AV deals with the sales and use tax related to aviation jet fuel, the W-2 addresses income tax withholdings, demonstrating the varied ways through which tax responsibilities are communicated to tax authorities.

The Schedule C (Form 1040) is utilized by sole proprietors to report profits or losses from a business they operate. This form is similar to the SU-451-AV, as both are tools for reporting specific financial activities to tax authorities. The SU-451-AV focuses on transactions related to aviation jet fuel, whereas Schedule C encompasses a broader array of business income and expenses. The specificity of the SU-451-AV to aviation fuel sales and use taxes illustrates the tailored approach tax authorities take to different sectors of the economy.

Form 1120 is the U.S. Corporation Income Tax Return, required for corporations to detail their income, gains, losses, deductions, and credits to determine their federal income tax liability. Like the SU-451-AV, which is specialized for aviation fuel transactions in Vermont, Form 1120 caters to the tax reporting needs of corporations. Both documents are pivotal in fulfilling tax obligations, though they cater to different subjects—the former to a specific type of transaction and the latter to corporate income.

The Form 1099-MISC is an informational return used to report miscellaneous income such as rents, royalties, prizes, and awards. It has a similarity to the SU-451-AV in the sense that both forms communicate specific types of transactions to tax authorities. The SU-451-AV's focus on aviation jet fuel sales and use tax contrasts with the broader application of the 1099-MISC, underscoring the diversity of reporting requirements tailored to various tax situations.

Form 4868 is an application for an automatic extension of time to file a U.S. individual income tax return. It shares with the SU-451-AV the principle of adhering to tax filing requirements, albeit its function is to provide taxpayers with more time to prepare their returns. While the SU-451-AV immediately deals with the reporting of taxes due for aviation jet fuel, Form 4868 addresses the need for additional time to gather information necessary for completing tax returns, showcasing the supportive mechanisms in tax administration for compliance.

The Sales and Use Tax Return form, specific to various states, closely resembles the SU-451-AV in its function of reporting sales, use tax, and remitting payments to the state. Both forms are integral to the tax reporting process, collecting necessary information on taxable transactions within a specific period. The distinction lies in the breadth of transactions covered; while a general Sales and Use Tax Return includes a wide range of taxable goods and services, the SU-451-AV specifically targets aviation jet fuel, illustrating the specialized nature of some tax forms.

When you are filling out the Form SU-451-AV for reporting Sales and Use Tax on Aviation Jet Fuel in Vermont, there are important steps you should follow to ensure accuracy and compliance with the Vermont Department of Taxes. Here are several dos and don'ts:

Dos:Remember, the importance of accurate and timely submission of the Form SU-451-AV cannot be overstated. It ensures compliance with state tax regulations and helps avoid potential fines or penalties for inaccuracies or late submissions.

Understanding tax forms can often be daunting, especially when dealing with specific areas such as aviation jet fuel taxes in Vermont. The Form SU-451-AV is a vital document for companies in this niche, but there are widespread misconceptions about its usage and requirements. Let's clarify some of these misconceptions:

In reality, this form is a supplement and must be submitted along with the primary Form SU-451, not as a standalone document.

The instructions explicitly state that amounts listed should exclude any local option sales tax, which is a separate consideration.

However, the SU-451-AV is exclusively for reporting taxes related to aviation jet fuel, not other fuel types.

Only an officer or authorized agent of the company can certify and sign this form, ensuring accountability and correctness of the information provided.

Contrary to this belief, the form can indeed be faxed to the Miscellaneous Tax Division, offering a convenient digital submission option.

Signing the form signifies that the officer or authorized agent has examined the return and believes it to be true, correct, and complete, subjecting themselves to penalties for perjury if found otherwise.

While it reports the sales and use tax on aviation jet fuel, other tax liabilities must be reported and paid via appropriate channels and forms.

The form has a Return Due Date, making timely submission crucial to avoid penalties or interest on late payments.

The reporting period is predetermined and indicated on the form, aligning with fiscal or calendar tax periods as defined by the Vermont Department of Taxes.

Amounts listed on the SU-451-AV should be included in the totals on specific lines of the primary Form SU-451, ensuring a comprehensive and consolidated tax return.

Understanding the nuances of tax forms and their requirements is crucial for compliance and the accurate reporting of liabilities. The Form SU-451-AV, specific to aviation jet fuel, is no exception, and clarifying these misconceptions helps ensure companies navigate their tax responsibilities with greater confidence and accuracy.

Understanding the SU-451-AV form is crucial for businesses dealing with aviation jet fuel sales and use tax in Vermont. Here are key takeaways to help navigate the form and its requirements.

By adhering to these key points, businesses can ensure compliance with Vermont's tax reporting requirements for aviation jet fuel, fostering a more straightforward and accurate tax process.

Vt State Tax Forms - Through its structured format, this form educates taxpayers on the nuances of Vermont tax law, promoting informed compliance.

Transmittal Form Dmv - It underscores the critical role of specificity and detail in legal complaints regarding personal safety threats.