Fill Out a Valid S 3M Vermont Form

Fill Out a Valid S 3M Vermont Form

In the dynamic landscape of Vermont's tax regulations, the S-3M Vermont form emerges as a crucial document for businesses engaged in manufacturing, publishing, research and development, and packaging sectors seeking sales tax exemptions. This specialized Sales Tax Exemption Certificate caters to the specifics under the sections 32 V.S.A. §9741(14), (15), (16), (24), outlining a clear path for organizations to navigate the often complex terrain of tax exemptions. The form, which must be furnished to the seller rather than the Vermont Department of Taxes, distinguishes between single and multiple purchase certificates, thereby accommodating both one-time and recurring business transactions. Key elements such as the buyer's and seller's details, the nature of the exemption claimed, and a certification of the information's accuracy by the buyer or authorized agent are integral to its structure. Additionally, the S-3M form sets the groundwork for operational efficiencies by highlighting the intended use of purchased goods – whether they be consumed in manufacturing, employed in research and development, or utilized in packaging. It insists on good faith acceptance by sellers, fortified by stringent criteria that protect both parties in the transaction. This framework not only facilitates a smoother procurement process for tangible personal property but also underscores the importance of compliance and due diligence in claiming tax exemptions, thus serving as an indispensable tool for eligible Vermont businesses.

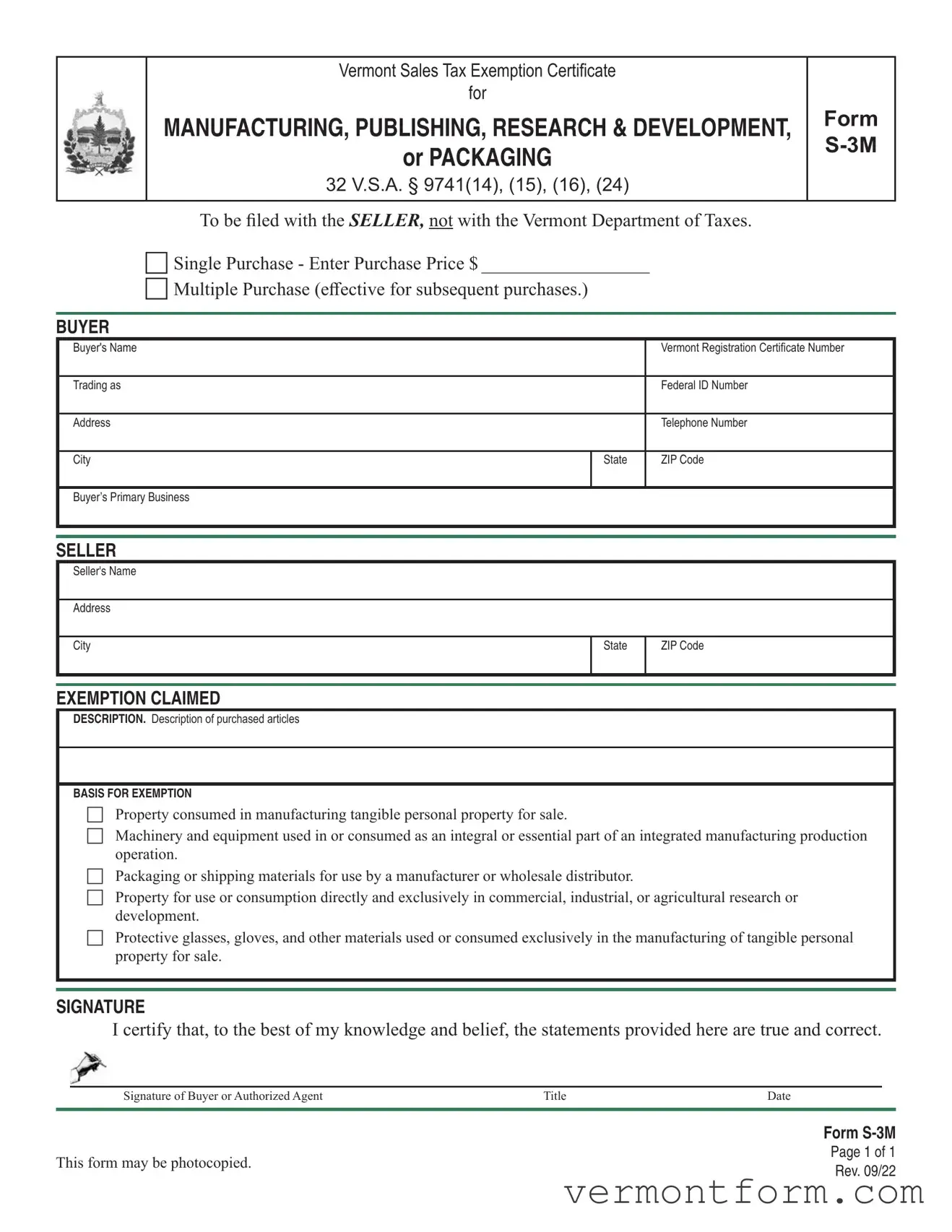

Vermont Sales Tax Exemption Certificate

for

MANUFACTURING, PUBLISHING, RESEARCH & DEVELOPMENT, FORM |

|

or PACKAGING |

|

|

|

32 V.S.A. § 9741(14), (15), (16), (24) |

|

To be filed with the SELLER, not with the Vermont Department of Taxes.

Single Purchase - Enter Purchase Price $ __________________

Multiple Purchase (effective for subsequent purchases.)

BUYER

Buyer's Name |

|

Vermont Registration Certificate Number |

|

|

|

Trading as |

|

Federal ID Number |

|

|

|

Address |

|

Telephone Number |

|

|

|

City |

State |

ZIP Code |

|

|

|

Buyer’s Primary Business |

|

|

|

|

|

|

|

|

SELLER

Seller's Name

Address

City |

State |

ZIP Code |

|

|

|

|

|

|

EXEMPTION CLAIMED

DESCRIPTION. Description of purchased articles

BASIS FOR EXEMPTION

Property consumed in manufacturing tangible personal property for sale.

Machinery and equipment used in or consumed as an integral or essential part of an integrated manufacturing production operation.

Packaging or shipping materials for use by a manufacturer or wholesale distributor.

Property for use or consumption directly and exclusively in commercial, industrial, or agricultural research or development.

Protective glasses, gloves, and other materials used or consumed exclusively in the manufacturing of tangible personal property for sale.

SIGNATURE

I certify that, to the best of my knowledge and belief, the statements provided here are true and correct.

Signature of Buyer or Authorized Agent |

Title |

Date |

Form

This form may be photocopied. |

Page 1 of 1 |

|

Rev. 09/22 |

||

|

FORM

Vermont Sales Tax Exemption Certificate for

Manufacturing, Publishing, Research & Development, or Packaging

General Information

Please print in BLUE or BLACK ink only.

Tangible personal property is property which can be seen, touched, and measured.

The term “distributor” does not include retailers selling directly to the ultimate consumer. Retail stores of all kinds and restaurants are not included in the terms “manufacturer” or “distributor.”

Tangible personal property that becomes an ingredient or component part of, or is consumed or destroyed in the manufacture of property for sale is exempt. Further, machinery and equipment used in or

consumed as an integral or essential part of an integrated production operation by a manufacturing plant is exempt. Where manufacturing begins and ends is described in 32 V.S.A. § 9741(14). Pre- manufacturing and

Form

Accepting an Exemption Certificate in “Good Faith”

The buyer must present to the seller an accurate and properly executed exemption certificate for the exempted sale. The responsibility is on the seller to determine if the buyer is submitting the exemption certificate in “good faith.” This requires the seller to be familiar with Vermont Sales and Use Tax law and regulations, including exemptions, that apply to the seller’s business. If the buyer provides a certificate that is not valid, i.e., the item purchased does not qualify for the exemption, this is not in good faith and the seller should not accept the certificate. When the seller accepts the certificate in good faith, the seller is not liable for collecting and remitting Vermont Sales Tax.

An exemption certificate is received at the time of sale in good faith when all of the following

conditions are met:

•The certificate contains no statement or entry which the seller knows, or has reason to know, is false or misleading.

•The certification is on an exemption form issued by the Vermont Department of Taxes or a form with substantially identical language.

•The certificate is signed, dated and complete (all applicable sections and fields completed).

•The property purchased is of a type ordinarily used for the stated purpose, or the exempt use is explained.

Form

Page 1 of 2 Rev. 09/22

Improper Certificate / Lack of Certificate

Sales transactions which are not supported by properly executed exemption certificates shall be deemed to be taxable retail sales. The burden of proof that the tax was not required to be

collected is upon the SELLER.

Retention of Certificates

Certificates must be retained by the seller for a period of not less than three (3) years from the date of the last sale covered by the certificate.

Additional Purchases by Same Buyer

If the buyer presents a “Multiple Purchase” exemption certificate to the seller, it may be used only when purchasing tangible personal property for use as indicated on this exemption certificate. For each purchase covered by the exemption certificate, the sales slip or invoice must show the buyer’s name and address sufficient to link the purchase to the exemption certificate on file.

Form

Page 2 of 2 Rev. 09/22

| # | Fact |

|---|---|

| 1 | The Vermont S-3M form is used for sales tax exemption specifically for manufacturing, publishing, research & development, or packaging as outlined in 32 V.S.A. §9741(14), (15), (16), (24). |

| 2 | This form must be filed with the seller, not with the Vermont Department of Taxes. |

| 3 | It allows for both single purchase exemptions and multiple purchase exemptions. |

| 4 | Qualifying purchases include machinery and equipment used directly and exclusively in manufacturing tangible personal property for sale, and packaging or shipping materials used by a manufacturer or wholesale distributor. |

| 5 | The form requires basic information about the buyer and seller, including names, addresses, and identification numbers. |

| 6 | The buyer certifies the truth and correctness of the information provided on the form. |

| 7 | Sellers must retain the certificates for at least three years from the date of the last sale covered by the certificate. |

| 8 | For buyers holding a multiple purchase certificate, additional purchases of the same type of property are covered without needing a new exemption certificate for each purchase. |

Filling out the S-3M Vermont Sales Tax Exemption Certificate is straightforward when you know what steps to follow. This form grants eligible manufacturers, publishers, researchers, and packagers specific tax exemptions for purchases related to their operations, as defined under Vermont laws. Accuracy and thoroughness are key when completing this document to ensure compliance and to legitimately claim your tax exemptions. Below is a step-by-step guide to assist you in the process.

Once the S-3M form is completely filled out, it should be filed with the seller, not with the Vermont Department of Taxes. Remember, this document may be photocopied, so keep a copy for your records. Holding onto this form for at least three years is mandatory as it supports your tax exemption claims during that period. Should you make additional purchases that fall under the same exemption claim and you've opted for the multiple purchases option, ensure each transaction is traceable back to the exemption certificate on file with the seller.

What is the purpose of the Vermont Sales Tax Exemption Certificate for Manufacturing, Publishing, Research & Development, or Packaging (S-3M)?

This certificate allows businesses in Vermont that are engaged in manufacturing, publishing, research and development, or packaging to purchase materials and equipment without paying state sales tax, provided these purchases meet specific criteria related to their business operations.

Who needs to file the S-3M form?

The buyer, who is conducting business in one of the applicable categories (manufacturing, publishing, research & development, or packaging), needs to fill out and provide this form to the seller at the time of purchase to claim exemption from sales tax.

Should the S-3M form be submitted to the Vermont Department of Taxes?

No, the completed form should not be submitted to the Vermont Department of Taxes. It must be kept on file by the seller for a period of at least three years from the date of the last sale covered by the certificate to document the tax-exempt transactions.

Can the S-3M form be used for multiple purchases?

Yes, the S-3M form can be designated for single or multiple purchases. If it is used as a Multiple Purchase certificate, it applies to subsequent purchases of the same type of property without needing to submit a new form for each purchase.

What types of property are covered under this exemption?

The exemption applies to property consumed in manufacturing tangible personal property for sale, packaging or shipping materials for use by a manufacturer or wholesale distributor, machinery and equipment used directly and exclusively in the manufacture, printing, or publishing of tangible personal property for sale, and property for use or consumption directly and exclusively in commercial, industrial, or agricultural research or development.

What is required for a seller to accept an exemption certificate in "good faith"?

To accept a certificate in "good faith", a seller must ensure that the certificate is complete, contains no misleading information, is substantially similar to the provided form, is dated and executed according to instructions, and that the property being purchased is of a type ordinarily used for the purpose described in the certificate. The certificate must also be received at or before the time of sale.

What happens if an exemption certificate is improperly filled out or not provided?

Sales transactions not supported by properly executed exemption certificates are considered taxable retail sales. The responsibility to prove that the tax was not required to be collected rests with the seller, highlighting the importance of obtaining and filing complete and accurate certificates.

Are there any specific items that do not qualify for the S-3M exemption?

Yes, activities and purchases related to pre-manufacturing and post-manufacturing, such as procuring raw materials, storing materials and finished goods after initial packaging, disposing of waste, environmental protection, and managing business operations, do not qualify for the S-3M sales tax exemption.

Filling out the Vermont Sales Tax Exemption Certificate, also known as Form S-3M, can sometimes be a complex process. Several common mistakes are made by individuals during this process, which can lead to the rejection of the application or complications in tax compliance. The following list outlines mistakes frequently encountered on this form:

Not specifying between a single purchase or multiple purchases often leads to ambiguity. The form allows for the selection, yet it is commonly overlooked.

Inaccurate information in the Buyer or Seller sections can result in processing failures. It's imperative to double-check these fields for correctness.

Failing to include the buyer’s primary business information, which helps in verifying the eligibility for tax exemption.

Omitting the VT Registration Certificate Number and Federal ID Number, which are crucial for identification and tax purposes.

Incorrectly identifying the exemption claimed without understanding the specific categories that qualify under Vermont Sales Tax Exemption law.

Not providing a detailed description of the property consumed in manufacturing or the specifics of how machinery and equipment are used directly and exclusively in the eligible processes.

Overlooking the signing and dating of the form by the buyer or authorized agent, thereby invalidating the document.

Not adhering to the instructions provided for manufacturing, publishing, research & development, or packaging certificate of exemption, leading to incomplete or incorrectly filled forms.

Assuming pre-manufacturing and post-manufacturing activities are covered under the exemption without consulting the pertinent regulations that delineate where the manufacturing process begins and ends.

Ignoring the requirement to retain certificates for a minimum of three years from the date of the last sale covered by the certificate, which is vital for record-keeping and potential audits.

The aforementioned mistakes are not exhaustive but represent areas where individuals frequently encounter issues. Attention to detail and a thorough understanding of the form’s requirements can mitigate these errors. It's worth noting that:

Engaging with the Vermont Department of Taxes’ website or directly reaching out can provide clarifications and additional guidance.

Proper execution of an exemption certificate necessitates a good faith effort from both the seller and the buyer to ensure all information is accurate and complete.

Legal compliance involves understanding that each section and checkbox on the Form S-3M serves a specific regulatory purpose and must be treated with careful consideration.

In sum, diligent completion of the tax exemption certificate, grounded in a comprehensive understanding of its stipulations, plays a crucial role in the successful navigation of the exemption process.

When handling the S-3M Vermont Sales Tax Exemption Certificate for manufacturing, publishing, research & development, or packaging, several other forms and documents often accompany or follow its use to ensure compliance and proper documentation for tax-exempt purchasing. These forms facilitate accurate reporting, compliance with state regulations, and efficient business operations.

Together, these forms and documents support the claims made on the S-3M Vermont Sales Tax Exemption Certificate. By maintaining a comprehensive record and providing necessary supplementary documentation, businesses can streamline their exemption claims and ensure compliance with the Vermont Department of Taxes. This process not only aids in regulatory adherence but also supports efficient and effective business operations.

The Uniform Sales & Use Tax Exemption/Resale Certificate (Multijurisdiction) is a document remarkably similar to the S-3M Vermont form. Like the Vermont form, it is used by purchasers to claim tax exemption on products that are bought for resale, manufacturing, or other exempt purposes. Both documents require detailed information about the buyer and seller, including their business names, addresses, and tax identification numbers. Additionally, they both necessitate a detailed explanation of why the purchased goods are exempt from sales tax, ensuring compliance with specific state tax laws.

Another document akin to the S-3M Vermont form is the Streamlined Sales and Use Tax Agreement Certificate of Exemption. This document also allows businesses to purchase goods without paying sales tax at the time of sale, provided the goods are used in a manner that qualifies for exemption under the participating states' tax laws. Much like the S-3M form, this certificate requires participants to denote the type of exemption being claimed and includes conditions such as the purchase of machinery for manufacturing. Both certificates play a pivotal role in the proper documentation and claiming of tax exemptions across multiple states.

The Manufacturing and Research & Development Equipment Exemption Certificate is an additional document with resemblances to the S-3M Vermont form. Specifically crafted for the exemption of goods used in manufacturing and R&D, this certificate outlines exemptions similar to those stated in the S-3M, such as machinery and equipment purchases. Both documents necessitate the buyer's declaration that the purchased goods qualify under specific exempt categories, emphasizing the direct use in manufacturing, research, or development.

The Farmer's Exemption Certificate is another form that shares similarities with the S-3M Vermont form, though it targets a different sector. This certificate allows farmers to purchase supplies and equipment exempt from sales tax, provided they are used directly in agricultural production. Like the S-3M form, the Farmer's Exemption Certificate requires detailed information about the buyer's business and an attestation to the accuracy of the information provided. Both forms serve as a means for qualified purchasers to legally avoid sales taxes on eligible transactions.

Last but not least, the Exemption Certificate for Government Agencies and Enrolled Tribal Members closely mirrors the structure and purpose of the S-3M Vermont form. This document is utilized by government entities and tribal members to purchase goods tax-free, provided such purchases are eligible under the law. Both this certificate and the S-3M require detailed buyer and seller information, and they necessitate a declaration of the purpose for which the goods are being purchased exempt from tax. Despite serving different demographic groups, the fundamental purpose and structure of these documents remain aligned with facilitating tax-exempt purchases.

When completing the S-3M Vermont Sales Tax Exemption Certificate for FORM MANUFACTURING, PUBLISHING, RESEARCH & DEVELOPMENT, or PACKAGING, it's crucial to be precise and accurate to ensure compliance and avoid issues. Below are key dos and don'ts to consider:

Understanding the Vermont Sales Tax Exemption Certificate, specifically the S-3M form, is crucial for businesses in manufacturing, publishing, research & development, or packaging. However, there are several misconceptions about the use and application of this form. Clearing up these misunderstandings ensures businesses can fully benefit from the tax exemptions it offers. Here are four common misconceptions:

Only for Single Purchases: Many believe the S-3M form is only applicable for a single, large purchase. In truth, the form allows for both single and multiple purchases. By selecting the "Multiple Purchase" option, businesses can continue to make subsequent purchases of the same type of property without needing to re-submit the form for each transaction.

Filing with the Vermont Department of Taxes: Another common mistake is the belief that the S-3M form should be filed with the Vermont Department of Taxes. The correct procedure is for the form to be filed with the seller, not the tax department. This process ensures that the seller has the necessary documentation to exempt the buyer from sales tax on qualifying purchases.

Limited to Manufacturing Sector: It's a misconception that the exemptions are strictly for businesses in the manufacturing sector. The S-3M form also applies to businesses involved in publishing, research and development, and packaging. This broader applicability supports a range of industries in benefiting from tax exemptions on necessary purchases.

Exemption Scope: Some assume the exemption only covers machinery and equipment. However, the S-3M form's scope includes not just machinery and equipment used directly and exclusively in manufacturing, but also packaging or shipping materials for use by a manufacturer or wholesale distributor, and property consumed in manufacturing tangible personal property for sale. This wide scope is designed to support various aspects of production and distribution.

Correctly understanding and applying the guidelines of the S-3M Vermont Sales Tax Exemption Certificate can significantly benefit qualifying businesses. It's essential to be aware of these common misconceptions to ensure your business takes full advantage of the tax exemptions provided under Vermont law.

Filling out and using the S-3M Vermont form, which is designed for tax exemptions in specific manufacturing, publishing, research and development, or packaging contexts, comes with several key points that both buyers and sellers need to be mindful of. These takeaways ensure compliance with Vermont tax laws and help streamline the process of claiming tax exemptions.

By paying close attention to these points, both buyers and sellers can navigate the complexities of tax exemptions in Vermont more effectively, ensuring they meet all legal requirements while taking advantage of the benefits offered by the S-3M form.

Vermont Nursing License - Your social security number or passport number is required for verification purposes, and safeguarded according to privacy laws.

Sales Tax in Vermont - Eligibility criteria require that the purchased property be ordinarily used by the buyer for purposes aligning with the exempt project's nature.

Su 451 Av - The direct connection of this supplemental form with the main SU-451 form ensures cohesive tax reporting.