Fill Out a Valid Eft 2 Form

Fill Out a Valid Eft 2 Form

The EFT-2 form serves as a crucial tool for businesses operating within Vermont, streamlining the tax remittance process through the ACH Credit payment system. Issued by the Vermont Department of Taxes, located at 133 State Street, PO Box 547, Montpelier, VT 05601-0547, this form specifically caters to those opting for the VTBIZFILE system. By allowing businesses to initiate payments directly from their bank accounts, the form not only facilitates a more efficient transfer of funds but also introduces a level of autonomy in managing tax dues. The completion and submission of this enrollment form is a straightforward yet vital process that enables businesses to take advantage of the ACH Credit method, which might incur charges by their respective banks, although the Vermont Department of Taxes does not impose any. Aside from bank information, the form requires basic company details such as the business name, federal ID number, and contact information, thereby simplifying the process. Upon submission and approval, businesses receive essential transaction information, including routing and banking numbers, alongside EFT codes necessary for successful payments. It is noteworthy that a test transmission with the bank is required to ensure accuracy before official use. This meticulous enrollment process underscores the importance of accuracy and compliance, paving the way for a seamless tax payment experience via the VTBIZFILE system. Furthermore, it aligns with modern financial practices by leveraging electronic funds transfer technology to enhance efficiency and security in tax payments.

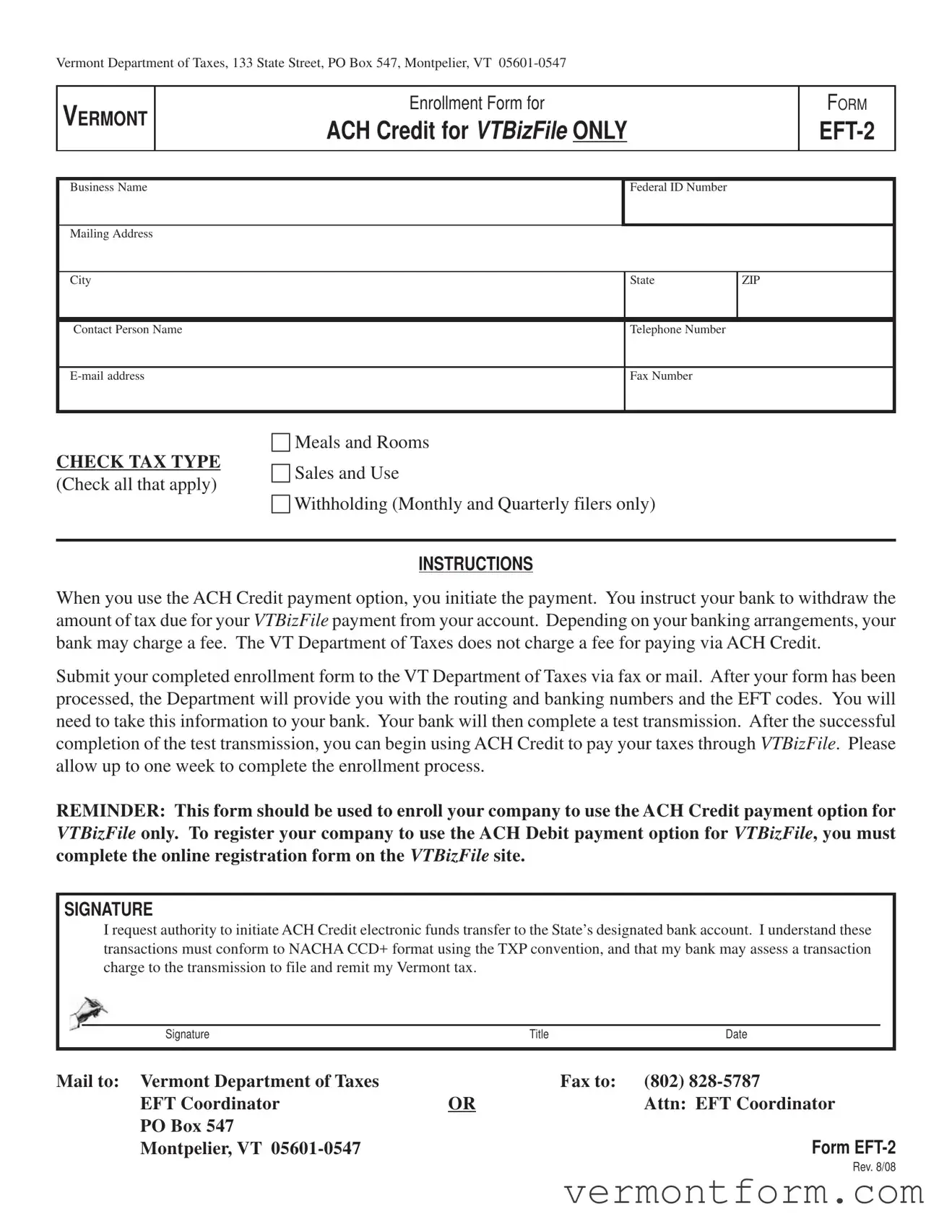

Vermont Department of Taxes, 133 State Street, PO Box 547, Montpelier, VT

VERMONT

Enrollment Form for

ACH CREDIT FOR VTBIZFILE ONLY

FORM

Business Name |

Federal ID Number |

|

|

|

|

Mailing Address |

|

|

|

|

|

City |

State |

ZIP |

|

|

|

Contact Person Name |

Telephone Number |

|

|

|

|

Fax Number |

|

|

|

|

|

Meals and Rooms

CHECK TAX TYPE

(Check all that apply)

Sales and Use

Withholding (Monthly and Quarterly filers only)

INSTRUCTIONS

When you use the ACH Credit payment option, you initiate the payment. You instruct your bank to withdraw the amount of tax due for your VTBIZFILE payment from your account. Depending on your banking arrangements, your bank may charge a fee. The VT Department of Taxes does not charge a fee for paying via ACH Credit.

Submit your completed enrollment form to the VT Department of Taxes via fax or mail. After your form has been processed, the Department will provide you with the routing and banking numbers and the EFT codes. You will need to take this information to your bank. Your bank will then complete a test transmission. After the successful completion of the test transmission, you can begin using ACH Credit to pay your taxes through VTBIZFILE. Please allow up to one week to complete the enrollment process.

REMINDER: This form should be used to enroll your company to use the ACH Credit payment option for VTBIZFILE only. To register your company to use the ACH Debit payment option for VTBIZFILE, you must complete the online registration form on the VTBIZFILE site.

SIGNATURE

I request authority to initiate ACH Credit electronic funds transfer to the State’s designated bank account. I understand these transactions must conform to NACHA CCD+ format using the TXP convention, and that my bank may assess a transaction charge to the transmission to file and remit my Vermont tax.

Signature |

Title |

Date |

|

|

|

Mail to: Vermont Department of Taxes |

Fax to: |

(802) |

EFT Coordinator |

OR |

Attn: EFT Coordinator |

PO Box 547 |

|

|

Montpelier, VT |

|

FORM |

Rev. 8/08

| Fact | Detail |

|---|---|

| Form Type | Enrollment Form for ACH Credit |

| Form Number | EFT-2 |

| Applicable State | Vermont |

| Governing Law | Vermont Department of Taxes Regulations |

| Purpose | To enroll companies to use ACH Credit for tax payments via VTBIZFILE |

| Address for Submission | Vermont Department of Taxes, 133 State Street, PO Box 547, Montpelier, VT 05601-0547 |

| Tax Types Supported | Meals and Rooms, Sales and Use, Withholding (Monthly and Quarterly filers only) |

| Submission Methods | Mail or Fax |

| Additional Information Required | Business Name, Federal ID Number, Mailing Address, Contact Person, Telephone Number, Email Address, Fax Number |

| Fees | No charge from VT Department of Taxes; possible bank fee |

Filling out the Form EFT-2 is a crucial step for businesses opting to pay their Vermont taxes through the ACH Credit system. This form enrolls your business into the system allowing you to control when payments are deducted from your account for tax obligations. Here's a step-by-step overview of what you need to include on the form to ensure a smooth enrollment process. Remember, taking these steps carefully can help avoid any delays or issues.

After your enrollment form is processed, the Vermont Department of Taxes will get in touch with the necessary routing and banking information along with the EFT codes. You will have to coordinate with your bank for a test transmission, and following a successful test, your business will be ready to utilize ACH Credit payments for your taxes. Remember to allow up to a week for the whole enrollment process to be completed.

What is the EFT-2 form used for in Vermont?

The EFT-2 form is an enrollment form for businesses in Vermont to sign up for ACH Credit payments specifically for VTBIZFILE. This allows businesses to pay their taxes electronically, directly from their bank account to the state’s designated bank account for tax types such as meals and rooms, sales and use, and withholding taxes for monthly and quarterly filers.

How does the ACH Credit payment option work?

When using the ACH Credit payment option, the business initiates the tax payment. This involves instructing their bank to transfer the specified tax amount from their bank account to the Vermont Department of Taxes. The business' bank may charge a fee for this service, though the Vermont Department of Taxes does not charge any fee for payments made this way.

What steps must be followed to enroll in the ACH Credit payment option?

First, complete the EFT-2 enrollment form and submit it via fax or mail to the Vermont Department of Taxes. After processing your form, the Department will provide you with necessary banking details. Take this information to your bank to conduct a test transmission. Following a successful test, you can start making ACH Credit payments for your taxes through VTBIZFILE.

What information is needed to fill out the EFT-2 form?

You will need your business name, Federal ID Number, mailing address, contact person's name, telephone number, email address, fax number, and the type of taxes your business is paying (e.g., meals and rooms, sales and use, withholding).

Is there a charge for using the ACH Credit payment option?

The Vermont Department of Taxes does not charge any fee for using the ACH Credit option. However, your bank might charge you a fee for processing the transaction. It is advisable to check with your bank regarding any potential charges before proceeding.

How long does it take to complete the enrollment process for ACH Credit?

The enrollment process for ACH Credit payments typically takes up to one week to complete. This time allows for the submission and processing of your EFT-2 form, as well as the necessary communication between your bank and the Vermont Department of Taxes.

Can I use the EFT-2 form to enroll for ACH Debit payments?

No, the EFT-2 form is specifically for enrolling in the ACH Credit payment option for VTBIZFILE. If you wish to use the ACH Debit payment option, you must complete the online registration form available on the VTBIZFILE site.

What are the tax types that can be paid using the EFT-2 form?

The EFT-2 form allows businesses to make electronic payments for several types of taxes, including meals and rooms tax, sales and use tax, and withholding tax (for both monthly and quarterly filers).

Where do I send the completed EFT-2 form?

The completed EFT-2 form should be mailed or faxed to the Vermont Department of Taxes. If mailing, send it to PO Box 547, Montpelier, VT 05601-0547. For fax submissions, the number is (802) 828-5787, attention to the EFT Coordinator.

Do I need to complete a test transmission before using ACH Credit?

Yes, after your enrollment form is processed and you have received the necessary banking information, your bank needs to complete a successful test transmission. This step ensures that the ACH Credit payments will be processed smoothly for your Vermont taxes.

When filling out the Vermont Department of Taxes EFT-2 Form for ACH Credit, it's crucial to avoid common mistakes to ensure the process is smooth and error-free. The EFT-2 form is a vital document for businesses opting to pay taxes via ACH Credit through VTBIZFILE. Here are ten mistakes frequently made:

Not checking all applicable tax types - The form allows the business to select the taxes they are enrolling in for ACH Credit. It is important to check all the boxes that apply to ensure all intended tax payments are processed correctly.

Incorrect business information - Filling in the wrong business name or Federal ID Number can lead to your payment being applied to the wrong account, or not at all.

Leaving contact details blank - The contact person's name, telephone number, and email address are crucial for communication. Omitting this information can result in delays if the Department needs to reach out for any clarification.

Forgetting to provide a complete mailing address - The city, state, and ZIP code are required to ensure all correspondence reaches you without delay.

Omitting fax number - Although not used as frequently, providing a fax number can be beneficial for faster communication in certain situations.

Not checking the appropriate box under "CHECK TAX TYPE" - This section is critical for specifying which taxes you're enrolling to pay via ACH Credit. An unchecked box means that tax type will not be processed through ACH Credit.

Skipping the signature - The form requires the signature of the person requesting the authority to initiate ACH Credit transactions. An unsigned form is not valid.

Leaving the Title and Date fields blank next to the signature - These fields are necessary to authenticate the signatory's authority and the date of request.

Incorrect routing and banking information - After receiving the routing and banking numbers from the Department, ensuring they are correctly relayed to the bank is crucial for the success of the test transmission and subsequent payments.

Not allowing enough time for enrollment process - Failing to account for the one-week processing time can lead to missed payments or late fees.

Correctly filling out the EFT-2 form is the first step to streamline your tax payments through ACH Credit. By avoiding these common mistakes, you can ensure a smoother process for your business and maintain compliance with the Vermont Department of Taxes.

When businesses opt to use the EFT-2 form for transactions, they're engaging in a streamlined process designed to manage their tax responsibilities efficiently. This form, dedicated to enabling ACH Credit payments for taxes, is just a part of the mosaic of documentation necessary for comprehensive financial and tax-related operations. Understanding the array of forms and documents that often accompany or complement the EFT-2 form can provide a clearer view of this landscape, demystifying the process for both new and seasoned entities in navigating their fiscal duties more effectively.

The navigation and proper filing of these forms, including and beyond the EFT-2, constitute a significant aspect of a business's compliance and financial operations. The interplay between them aids in the holistic management of tax obligations, a crucial component for the financial health and legal standing of any business entity. By familiarizing themselves with these documents, businesses can ensure they meet their responsibilities efficiently and effectively, contributing to a seamless operation within the regulatory frameworks.

The Form EFT-2, utilized for enrolling in the ACH Credit payment option for tax payments through VTBIZFILE in Vermont, shares similarities with the IRS Form 940, which is the Federal Unemployment Tax Act (FUTA) Tax Return. Both forms involve the management of business taxes and require detailed business information, including the federal ID number and business name. However, while the EFT-2 form relates to electronic transactions for tax payments, Form 940 is used specifically for reporting annual federal unemployment taxes.

Another document resembling the EFT-2 form is the Form 941, the Employer's Quarterly Federal Tax Return. This form is essential for reporting income taxes withheld from employees' paychecks, along with reporting Social Security and Medicare taxes owed by employers and employees. Like the EFT-2, Form 941 deals with regular tax duties of businesses and necessitates accurate financial and identification information. Differences lie in the frequency of submission and specific tax types each form addresses.

The EFTPS Enrollment Form is also akin to the EFT-2 form. The Electronic Federal Tax Payment System (EFTPS) is a service provided by the U.S. Department of the Treasury for paying federal taxes electronically. Both forms facilitate the setup of electronic payments for taxes, though the EFTPS Enrollment Form is broader, allowing for various federal tax types, while the EFT-2 is specifically for certain state taxes in Vermont.

A resemblance is found with the Sales and Use Tax Return forms that many states use for businesses to report and pay taxes collected from customers. Similar to the EFT-2, these forms require business identification details and involve tax transactions. The primary difference revolves around the EFT-2's role in setting up electronic payments, whereas sales and use tax forms typically encompass the reporting and calculation of the taxes owed.

The State Withholding Tax Forms, which businesses use to report and pay state income taxes withheld from employees' wages, also share features with the EFT-2 form. Both types of documents are crucial for tax compliance by businesses, including the necessity for the business's identifying information. The core distinction is that the EFT-2 form focuses on the electronic payment setup, whereas withholding tax forms are more about the reporting of employees' withholdings.

Form W-2, the Wage and Tax Statement, parallels the EFT-2 in its involvement in the realm of taxation. Employers use Form W-2 to report total annual wages earned by employees and the taxes withheld from their paychecks. Though serving different functions—one for enrollment in electronic tax payments and the other for annual wage reporting—both demand detailed employer and employee information to ensure proper tax handling.

The Form W-3, Transmittal of Wage and Tax Statements, serves a companion role to the W-2 by summarizing employee earnings, taxes withheld, and Social Security and Medicare taxes owed. It resembles the EFT-2 form in its aggregation of tax-related information for submission to a tax authority. However, its purpose diverges in that it focuses on summarizing and transmitting already calculated tax information.

The Direct Debit Installment Agreement (DDIA) form, utilized by taxpayers to set up payment plans for their tax liabilities via direct debits, exhibits similarities to the EFT-2 form. Both facilitate the electronic transfer of funds for tax payments, ensuring that taxpayers or businesses can manage their obligations efficiently. The distinction lies in the EFT-2's use for businesses making state tax payments and the DDIA's aim towards individual taxpayers arranging payment plans for outstanding taxes.

Business Registration forms, required for a new business to officially register with state tax authorities, share commonalities with the EFT-2 form. These registration forms collect comprehensive business details and establish the business's tax account with the state. The comparison is apparent in the collection of business information, though the purposes differ: the EFT-2 enrolls a business in an electronic payment method, while registration forms typically mark the business's initial setup in the state's tax system.

Finally, the Change of Address or Responsible Party — Business form, which businesses file to notify tax authorities of changes in address or primary contacts, bears resemblances to the EFT-2 form. Both require current business information and ensure that records are up to date to facilitate proper tax administration. While the EFT-2 form is specific to enrolling in electronic payments, the Change of Address form focuses on maintaining accurate records for communications and tax processing purposes.

When completing the Vermont Department of Taxes Form EFT-2 for ACH Credit enrollment, it is critical to approach the process with attention to detail to ensure accurate and efficient processing. Below are guidelines to help you navigate the submission correctly and avoid common pitfalls.

Do:

Don't:

Understanding the Vermont Department of Taxes Form EFT-2 comes with its own set of challenges, often leading to misconceptions. Here are five common ones:

Understanding these nuances ensures that businesses can navigate their tax payments with clarity and confidence, leveraging the ACH Credit option efficiently.

Understanding the basics of the EFT-2 form is crucial for businesses opting to use the ACH Credit method for their Vermont tax payments. Here are the key takeaways:

It's essential for any business engaging with this form to carefully follow the instructions and requirements to prevent any delays or issues with their tax payments. The process, while straightforward, requires attention to detail to ensure all financial and tax transactions are conducted smoothly and efficiently.

Vermont 813B - Filing the 813B form before the first case manager's conference or court hearing is critical for timely compliance within the legal process.

What Is an Amendment in Real Estate - It is an important tool for clarifying the full extent of what the buyer is receiving beyond the real estate itself.