Fill Out a Valid E2A Form

Fill Out a Valid E2A Form

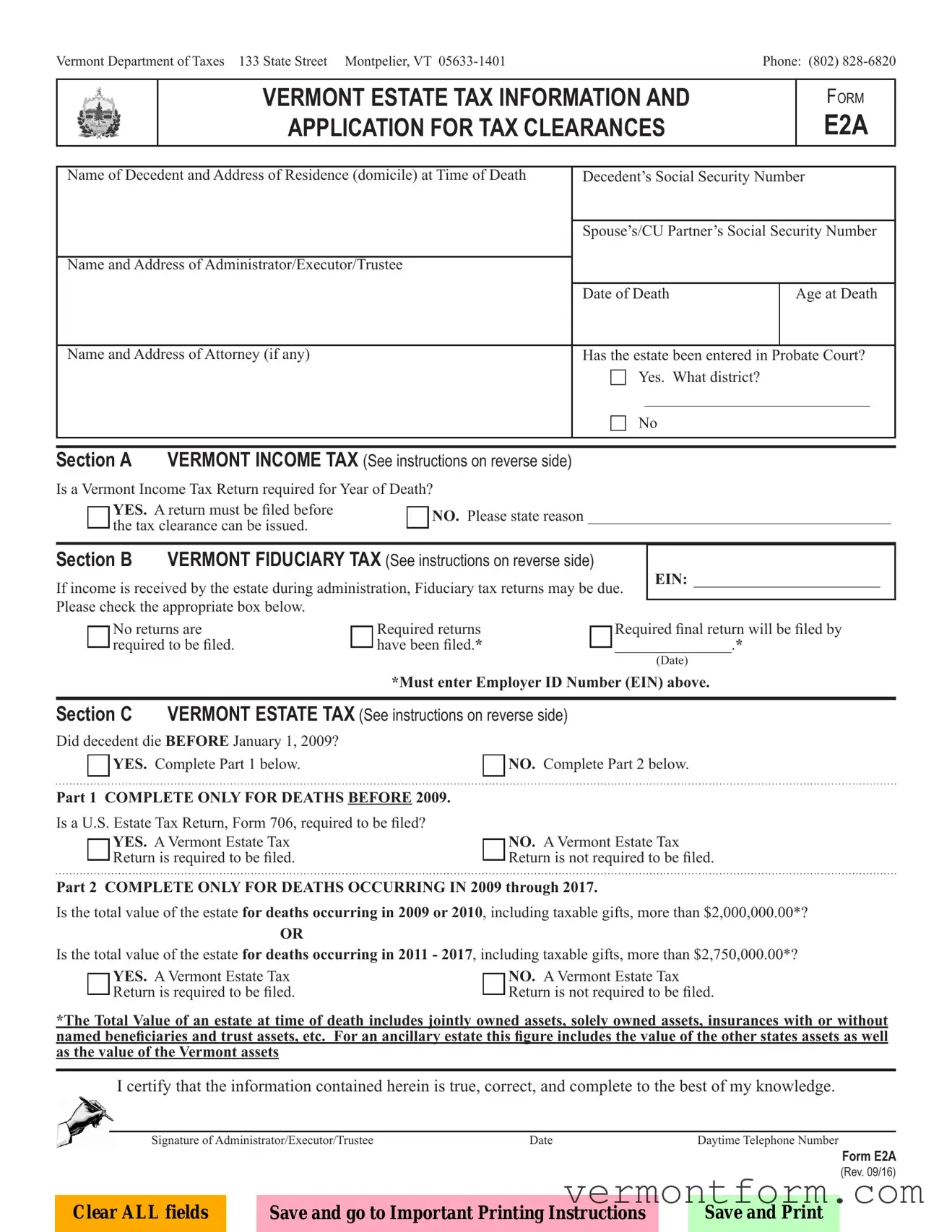

When navigating the aftermath of a loved one's passing in Vermont, the logistics of estate management loom large, accentuated by the requirement to settle estate taxes efficiently. The Vermont Department of Taxes provides critical guidance via the Form E2A, an essential document for those managing the decedent's financial responsibilities. Primarily, this form serves as an application for tax clearances, focusing on Vermont Estate, Income, and Fiduciary Taxes. It requires detailed information about the decedent, including their Social Security number, domicile at the time of death, and the appointed administrator or executor's details. Importantly, the form distinguishes between estates of individuals who passed before and after January 1, 2009, stipulating different criteria for each to determine the necessity of filing a Vermont Estate Tax Return. Furthermore, it inquires whether a Vermont Income Tax Return is required for the year of death and if fiduciary tax returns are due because of income received by the estate during administration. The necessity of completing this form underlines the importance of transparency and compliance in estate management, ensuring the decedent's affairs are settled according to state laws and regulations.

Vermont Department of Taxes 133 State Street Montpelier, VT

|

VERMONT ESTATE TAX INFORMATION AND |

Form |

||||

|

APPLICATION FOR TAX CLEARANCES |

E2A |

||||

|

|

|

|

|

|

|

Name of Decedent and Address of Residence (domicile) at Time of Death |

Decedent’s Social Security Number |

|||||

|

|

|

|

|

|

|

|

|

|

Spouse’s/CU Partner’s Social Security Number |

|||

|

|

|

|

|

|

|

Name and Address of Administrator/Executor/Trustee |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Date of Death |

|

Age at Death |

|

|

|

|

|

|

|

|

Name and Address of Attorney (if any) |

|

Has the estate been entered in Probate Court? |

||||

|

|

|

Yes. What district? |

|

||

|

|

|

_ _____________________________ |

|||

|

|

|

No |

|

||

|

|

|

|

|

||

|

|

|

|

|

||

Section A VERMONT INCOME TAX (See instructions on reverse side) |

|

|

|

|||

Is a Vermont Income Tax Return required for Year of Death? |

|

|

|

|||

YES. A return must be filed before |

NO. Please state reason________________________________________ |

|||||

the tax clearance can be issued. |

||||||

|

|

|

|

|||

Section B VERMONT FIDUCIARY TAX (See instructions on reverse side)

If income is received by the estate during administration, Fiduciary tax returns may be due. Please check the appropriate box below.

EIN:_ ________________________

No returns are required to be filed.

Required returns have been filed.*

Required final return will be filed by

_______________.*

(Date)

*Must enter Employer ID Number (EIN) above.

Section C VERMONT ESTATE TAX (See instructions on reverse side)

Did decedent die BEFORE January 1, 2009?

YES. Complete Part 1 below.

YES. Complete Part 1 below.

Part 1 COMPLETE ONLY FOR DEATHS BEFORE 2009.

Is a U.S. Estate Tax Return, Form 706, required to be filed? YES. A Vermont Estate Tax

Return is required to be filed.

NO. Complete Part 2 below.

NO. Complete Part 2 below.

NO. A Vermont Estate Tax Return is not required to be filed.

Part 2 COMPLETE ONLY FOR DEATHS OCCURRING IN 2009 through 2017.

Is the total value of the estate for deaths occurring in 2009 or 2010, including taxable gifts, more than $2,000,000.00*?

OR

Is the total value of the estate for deaths occurring in 2011 - 2017, including taxable gifts, more than $2,750,000.00*?

YES. A Vermont Estate Tax |

|

NO. A Vermont Estate Tax |

|

||

Return is required to be filed. |

|

Return is not required to be filed. |

|

*The Total Value of an estate at time of death includes jointly owned assets, solely owned assets, insurances with or without named beneficiaries and trust assets, etc. For an ancillary estate this figure includes the value of the other states assets as well as the value of the Vermont assets

I certify that the information contained herein is true, correct, and complete to the best of my knowledge.

Signature of Administrator/Executor/Trustee |

Date |

Daytime Telephone Number |

Form E2A

(Rev. 09/16)

Clear ALL fields |

|

Save and go to Important Printing Instructions |

|

Save and Print |

|

|

|

|

|

| Fact | Detail |

|---|---|

| Purpose of Form E2A | Application for Tax Clearances related to Vermont Estate Tax, Vermont Income Tax for the Decedent, and Vermont Fiduciary Tax. |

| Governing Law | Vermont State Law, specifically pertaining to estate taxation and the required filings post-death. |

| Estate Valuation Thresholds for Tax Requirement | For deaths occurring in 2009 or 2010, an estate valued over $2,000,000.00 requires filing. For deaths between 2011 and 2017, the threshold is $2,750,000.00. |

| Deadline Precedence | A Vermont Income Tax Return must be filed for the year of the decedent's death before tax clearance can be issued. |

| Fiduciary Returns Relevance | If the estate receives income during administration, Fiduciary Tax Returns may be necessary. |

After the passing of a loved one, navigating through legal documents is a significant step towards finalizing their affairs. The Vermont Estate Tax Information and Application for Tax Clearances E2A form is critical for executors or administrators to ensure compliance with state tax obligations. Completing this form is a diligent process that involves providing detailed information about the decedent and their estate. Here are the steps you need to follow to accurately fill out the E2A form.

Once the form is completed and checked for accuracy, it should be saved. Follow the necessary steps to print the document as per the important printing instructions. This form will play a crucial role in ensuring the estate is handled according to Vermont state laws, and it is essential to approach this task with attention to detail and care.

Welcome to the FAQ section regarding the Vermont Estate Tax Information and Application for Tax Clearances, Form E2A. This section aims to provide answers to some common questions you might have while filling out or understanding the E2A form.

The E2A form is used by the Vermont Department of Taxes for estate tax clearances in Vermont. It collects information about the decedent, such as name, address at time of death, and Social Security Number, along with details about the estate's administrator or executor, and whether estate, fiduciary, and income taxes have been filed or are required.

If you are the administrator, executor, or trustee of an estate with a decedent who was a resident of Vermont at the time of death, you might need to complete the E2A form. This includes determining and stating the necessity of filing Vermont income tax, fiduciary tax, and estate tax returns.

A Vermont Income Tax Return must be filed for the year of death before tax clearance can be issued if the deceased was a resident or earned income in Vermont. The E2A form specifically asks if a return is necessary and, if not, requires an explanation.

After a person's death, if their estate generates income during administration, it may be subject to Vermont fiduciary tax. This is declared in Section B of the E2A form, where it must be indicated whether fiduciary tax returns are required, have been filed, or when they will be filed.

The necessity for a Vermont Estate Tax Return is based on the total value of the estate at the time of death, including jointly owned assets, solely owned assets, insurance proceeds, and trust assets. The thresholds vary by the year of death, affecting estates of decedents dying before 2009, in 2009 or 2010, and from 2011 - 2017.

The requirements for filing differ based on the date of death. If the decedent died before January 1, 2009, certain parts of the E2A form must be completed. For deaths occurring from 2009 through 2017, other criteria regarding the estate's total value apply.

An Employer Identification Number (EIN) is necessary if estate income is received during its administration, as indicated in Section B concerning Vermont Fiduciary Tax.

Yes, the E2A form provides options to clear all fields, save your progress for later completion, and instructions for printing. This ensures that information can be reviewed and corrected before submission to the Vermont Department of Taxes.

For further assistance or specific questions not covered in this FAQ, the Vermont Department of Taxes can be contacted at (802) 828-6820. Their office is located at 133 State Street, Montpelier, VT 05633-1401.

It's crucial to thoroughly review the E2A form and its instructions to ensure compliance with Vermont's tax laws and requirements. For legal advice or more detailed information, consulting with a tax professional or attorney is recommended.

When completing the Vermont E2A form for tax clearances, it is imperative to pay attention to detail to avoid common mistakes. The following outlines the mistakes frequently made by individuals during this process:

In conclusion, diligently reviewing all sections of the Vermont E2A form, ensuring accurate and complete information, and understanding the specific requirements based on the decedent's date of death and the value of their estate are pivotal steps in submitting a successful application for tax clearances.

Understanding the documentation involved in estate management, especially after the loss of a loved and the necessity to deal with taxes and legalities, can be daunting. The Vermont Estate Tax Information and Application for Tax Clearances, known as the E2A form, serves as a critical tool in this process. However, handling an estate usually requires more than just this single form. Below is a list of additional documents and forms often used alongside the E2A to ensure comprehensive estate management and tax compliance.

The preparation and filing of these documents can be complex and often require a keen understanding of both federal and state laws. Professionals such as attorneys, accountants, and tax advisors play an essential role in guiding executors or administrators through this process. It's not just about fulfilling legal obligations but also about honoring the decedent's wishes in the most respectful and efficient manner possible.

The Form 1040, commonly utilized for individual income tax returns in the United States, shares similarities with the Vermont E2A form in its function of reporting financial information to a tax authority. Both forms require the submission of personal identifiers, such as Social Security numbers and addresses, and ask for detailed financial data to determine the tax obligations of the individual or estate. While the E2A form focuses on estate tax clearances, including income and fiduciary tax aspects related to a decedent's estate, the 1040 form captures an individual's yearly income, deductions, and credits to calculate owed federal income tax.

The Form 706, or the United States Estate (and Generation-Skipping Transfer) Tax Return, has a clear parallel to the Vermont E2A form, especially where the E2A requires information to determine if a Vermont Estate Tax Return is necessitated by the decedent's financial circumstances at the time of death. Both documents are concerned with the valuation of an estate to assess tax responsibilities arising from transfers of wealth at death, including the enumeration of assets, deductions, and computing tax due, based on the value of the estate and applicable tax rates or exemptions.

Form 1041, the U.S. Income Tax Return for Estates and Trusts, mirrors the fiduciary section of the E2A form, as both are dedicated to capturing the income tax obligations of estates or trusts. These documents collect information about income generated by the estate or trust, allowable deductions, and the resulting income tax liability. The need to provide an Employer Identification Number (EIN) and indicate whether fiduciary income tax returns are required mirror each other in both the structure and intent of ensuring proper taxation of income generated before the distribution to beneficiaries.

The Application for Tax Clearance Certificate, often a requisite in finalizing the affairs of deceased individuals or dissolved entities, parallels the E2A's purpose. While the Vermont-focused E2A form specifically facilitates the process of settling estate taxes and ensuring compliance with state tax obligations before distributing assets, a Tax Clearance Certificate generally serves a broader purpose. It provides official proof that a taxpayer's affairs are in order with a particular tax authority, be it for estate, individual, or corporate taxes, affirming that all tax liabilities have been satisfied.

Lastly, the similarity between the Vermont E2A form and state-specific inheritance tax return forms, where applicable, illustrates another aspect of posthumous financial settlement. Inheritance tax, distinct from estate tax, is levied in some jurisdictions based on the value of specific inheritances to individual beneficiaries. Forms like the E2A that encompass estate tax assessment might not directly address inheritance tax but share the commonality of facilitating tax compliance following a death, in terms of evaluating the financial assets and obligations of the deceased and ensuring appropriate taxation based on those assets.

When filling out the E2A form for the Vermont Department of Taxes, it’s important to navigate the process accurately and thoroughly to ensure compliance and to expedite the tax clearance for an estate. Here are some dos and don’ts to consider:

When handling the Vermont E2A form for estate tax information and application for tax clearances, it's easy to stumble over a few misconceptions. Let's clear up some of the most common misunderstandings:

Any estate regardless of its value must file the E2A form. This is not true. Whether an E2A form needs to be filed depends on the total value of the estate. Specific thresholds must be met before filing is required, which varies depending on the year of death.

The E2A form is only for estates of deceased Vermont residents. While it's primarily used by Vermont residents, it also applies to non-residents who owned property in Vermont or had other taxable estate elements within the state.

Filing the E2A form negates the need for a federal estate tax return. This is a misconception. The need to file a federal estate tax return, Form 706, is separate and governed by federal regulations, which may apply regardless of the requirement to file an E2A form in Vermont.

There’s no need to file a return if the decedent did not have a high-income level. The requirement to file a Vermont estate tax return does not hinge solely on the income level of the decedent, but rather on the total value of the estate, among other factors.

The filing of an E2A form automatically grants tax clearance. Submitting the form is a step in the process, but tax clearances are issued only after the Vermont Department of Taxes reviews and approves the submission based on its compliance with state tax laws and regulations.

All sections of the E2A form must be completed for every estate. Not every section applies to every estate. For instance, Parts 1 and 2 of Section C ask questions based on the decedent's year of death, and only the relevant part should be completed.

If no estate tax return is required, then the estate is cleared of all Vermont taxes. Not necessarily. The estate may still be responsible for other taxes, such as income or fiduciary taxes, even if no estate tax return is required.

The information on the E2A form does not need verification. On the contrary, the administrator, executor, or trustee certifies that the information provided is true, correct, and complete, highlighting the importance of accuracy.

An attorney's involvement is mandatory in completing the E2A form. Although having an attorney can be very helpful, especially in complex cases, it is not a mandatory requirement for completing the form.

The E2A form covers all taxes related to the estate. The E2A form is specific to estate taxes and applications for tax clearances. It does not encompass all potential taxes an estate may owe, such as property or income taxes on behalf of the decedent or the estate itself.

Understanding these nuances can help in correctly handling estate matters in Vermont, ensuring compliance and potentially easing the administrative burden on those dealing with a loved one's estate.

Completing the Vermont E2A form accurately is crucial in managing a deceased's financial affairs and ensuring compliance with state tax obligations. Here are key takeaways to guide you through this process:

Finally, the certification by the Administrator/Executor/Trustee that the information provided is true, correct, and complete underscores the importance of diligence and accuracy throughout the process. Involving an attorney may be advisable to ensure all legal and tax considerations are properly addressed.

Vermont 813B - Transfer or sale of assets within the last 12 months must be reported, highlighting any changes in financial status or attempts to conceal assets.

Sales Tax in Vermont - The distinction between single and multiple purchase certificates allows flexibility for contractors in managing project-related acquisitions.

Vermont Board of Pharmacy License Verification - Preparation tips for out-of-state pharmacies regarding the Vermont licensure application, focusing on accurate disclosures of ownership and management.